Introduction

On the 28th of February, the United States and Israel launched a surprise attack on Iranian military and government sites. The strikes resulted in civilian casualties and the deaths of several high-ranking officials, including Iran’s supreme leader, Ayatollah Ali Khamenei. The attack took place while negotiations over Iran’s nuclear program were ongoing. The Omani Foreign Minister, acting as intermediary between the US and Iran had just claimed a major diplomatic breakthrough: Iran was allegedly willing to pledge never to possess weaponisable nuclear material, commiting to zero stockpiling, irreversibly convert existing stockpiles into civilian fuel, and grant full IAEA access, even allowing American inspectors.

However, the US dismissed these developments and chose to attack, claiming that Iran was merely using the negotiation as a stalling tactic to mask an existential threat. Iran responded to the US strikes by attacking US bases across the Persian Gulf, Israeli cities, and US-allied Gulf-state infrastructure, warning that if Iranian ports were unsafe, no port in the Persian Gulf would be safe. Iran also imposed a blockade of the Strait of Hormuz, preventing the export of critical commodities such as crude oil, natural gas, phosphorus, ammonia, and helium. This blockade has especially affected countries to the east of Suez that depend on Persian Gulf states to supply these critical goods.

Beyond energy, a supply crisis is also brewing across the agricultural, semiconductor, and product packaging sectors, as the inputs and feedstocks for these industries are petroleum-related and are primarily supplied from that region. Despite being a net energy exporter, Malaysia is not immune; according to the Petronas Group CEO, the country still relies on the Persian Gulf for 40% of its oil imports. In Malaysian consumers’ minds, the immediate concern is the cost of petrol and diesel, as most Malaysians own private motor vehicles. Since energy is an important economic input, and West Asia remains its primary producer, understanding the regional politics that triggered this crisis is imperative. Additionally, any assessment of vulnerability must evaluate Malaysia’s preparedness to handle such a disruption. In what follows, we will look at these two issues to better understand the energy crisis we currently face.

Historical Genesis: 1953 to the 1979 Revolution

This war is a culmination of fraught relations between the US-Israel alliance and Iran, the origins of which could be traced to the 1950s. In 1953, the US orchestrated a coup against Iran’s democratically elected Prime Minister, Mohammed Mossadegh, following his nationalisation of the Anglo-Iranian Oil Company. To ensure that British and American interests were protected, both powers backed Mohammad Reza Pahlavi as the new Shah of Iran. The Shah, frequently derided as “The American Puppet”, was established as an authoritarian ruler over the Iranian government and its people, sustained by American weapons paid for by petrodollars and enforced by a brutal CIA-trained security service, SAVAK.

With the Shah aligned with Washington, the United States integrated Iran into its regional security architecture, making it a reliable ally to check Soviet influence and secure the safe passage of oil through the Strait of Hormuz. However, the Shah’s violent authoritarianism, exemplified by SAVAK's systemic imprisonment and torture of revolutionary leaders, alongside unpopular, forced secularisation policies, fuelled deep resentment and hostility among both the public and government officials. This anger was directed not only at the Shah but also at his American backers, who actively guided his domestic policies.

The deep-seated anger and exasperation against the Shah and foreign influence found an eloquent and charismatic spokesperson in Ayatollah Khomeini, the leader of the 1979 Iranian Islamic Revolution. Khomeini’s message resonated not just among traditionally religious communities, but across virtually all segments of Iranian society, outside the Shah’s immediate circle. The 1979 revolution garnered widespread public support because, among other promises, Khomeini pledged absolute economic, political, and cultural independence (Esteqlal). Khomeini and his fellow revolutionaries were not just against foreign influence but explicitly anti-American, a hostility forged by decades of US interference, and expressed during the fervour of revolution through anti-imperialist chants such as “Death to America”.

From that point onward, Washington viewed the Islamic Republic as a fanatical, ideological, and volatile actor incapable of making rational calculations and strongly opposed its ascension to power. Viewing itself as the rightful global hegemon, the United States saw the new government as a direct challenge to its regional primacy since Tehran refused to submit to the US-led order. The revolution permanently severed the close alliance between Iran and the US, and the fragile post-revolutionary dynamic turned overtly hostile after President Jimmy Carter admitted the deposed Shah into the US, ostensibly for medical treatment. Islamist-leaning students, fearing this move was a ruse to orchestrate a repeat of the 1953 coup, stormed the US embassy in Tehran in November 1979, seizing the compound and holding 52 American diplomats hostage. For the revolutionaries, the embassy seizure was a defensive bargaining tactic designed to force a commitment from Washington that it would no longer subvert or attack the newly formed Islamic Republic.

Escalation, Covert Alignments, and the Nuclear Question

The prospect of rapprochement has since grown slimmer following the US harbouring of the Shah and the hostage incident. In response to the embassy seizure, Washington imposed an import embargo on Iranian oil and froze USD12 billion in Iranian state assets to exert economic leverage while at the same time pursuing backchannel negotiations. The two nations finally reached an agreement through the Algiers Accord in January 1981, resulting in the release of the American hostages after 444 days in captivity. In exchange, the Islamic Republic secured a US commitment to non-intervention in its internal affairs and the return of its frozen assets. However, the deep mutual distrust and paranoia forged by the two incidents proved permanent.

Events throughout the 1980s further poisoned the relationship. In 1980, less than a year after the revolution, Iraq invaded Iran, igniting a brutal eight-year war. Determined to protect its strategic interest in West Asia and prevent the spread of Iranian influence to in the region, Washington covertly provided Baghdad with intelligence, financial backing, and logistical support. In doing so, the US deliberately turned a blind eye to Iraq’s deployment of chemical weapons, flagrantly violating its own pledges of non-intervention. Ironically, the Reagan administration simultaneously engaged in secret arms sales to Tehran, in exchange for Iranian assistance in securing the release of American and French hostages held by Hezbollah in Lebanon.

The covert arrangement, exposed as the Iran-Contra affair, ignited massive domestic controversy. The Reagan administration was caught not only dealing with Iran, which they themselves classified as a state-sponsor of terrorism, but also funnelling the profits from those arms sales to illicitly finance the Contras, an anti-communist Nicaraguan rebel group explicitly barred from receiving US funds by Congress. By the late 1980s, the two countries engaged in direct military clashes during the “Tanker War” in the Persian Gulf. This culminated in the tragic 1988 incident where a US cruiser shot down an Iranian civilian airliner, killing all 290 people on board. The disaster solidified an Iranian conviction that the US would stop at nothing to ensure their defeat.

Tentative attempts at reconciliation emerged in the 1990s under Iranian presidents Rafsanjani and Khatami, but domestic hardliners on both sides consistently scuttled these openings. Even under the strain of the Clinton administration’s dual containment policy, which threatened secondary sanctions on any oil company investing in Iran, Tehran offered unprecedented, unconditional cooperation to Washington following the September 11 attacks. Seeking to topple the Taliban, Iran provided critical intelligence, search-and-rescue assistance, and proxy ground forces. This tactical alignment was abruptly severed just weeks later when President George W. Bush designated Iran as part of the “Axis of Evil”.

The defining flashpoint leading to the 2026 Hormuz Crisis occurred in 2002, when an Israeli-linked dissident exposed covert nuclear facilities at Natanz and Arak, which the International Atomic Energy Agency (IAEA) had not yet been notified. This discovery raised alarms in Washington, raising fears of a self-sufficient, diversified nuclear weapons program. Technically, Iran had not breached any international agreements at the time. Under the safeguards then in force, Tehran was only required to declare new facilities six months prior to introducing nuclear material - a threshold it had not yet crossed. Though Iran immediately granted the IAEA full access upon request, Washington had already made Iran’s nuclear program the centre of its security concerns.

Dismissing Tehran’s subsequent overtures to negotiate comprehensive security differences, the US launched a sweeping sanctions campaign. Washington targeted nuclear-related entities first before expanding to “blocking sanctions” aimed directly at Iranian financial institutions. These measures effectively locked Iran out of the global banking system, as any foreign bank caught transacting with Iranian-related entities faced punishing US fines. Foreign banks complied strictly because access to the US market is indispensable, and losing access to the US dollar would cripple their ability to conduct international transactions, even those denominated in other currencies, since all currency pairs are, in actuality, intermediated by the USD through US-based accounts.

From the JCPOA Framework to Maximum Pressure

During President Obama’s term, the US initially extended a diplomatic hand to Iran but quickly backtracked after discovering that Iran was building an unannounced nuclear enrichment site at Fordow. Obama then pivoted to a comprehensive strategy that featured unprecedented economic coercion to force Iran to the negotiating table. The economic pressure took the form of severe secondary sanctions on foreign companies investing in Iran via CISADA 2010, alongside the 2011 Menendez-Kirk amendment. This targeted the Central Bank of Iran and forced international buyers to significantly reduce their purchase of Iranian oil or face exclusion from the US financial system.

The resulting economic isolation brought Hassan Rouhani to power in 2013, a figure more open to negotiating with the US than his immediate predecessor, Ahmadinejad. Rouhani’s negotiations with world powers culminated in the 2015 Joint Comprehensive Plan of Action (JCPOA), under which the West lifted nuclear-related secondary sanctions in exchange for Iran dismantling most of its centrifuges, surrendering 98% of its enriched uranium stockpile, and submitting to rigorous 24/7 international inspections.

When Trump came to power, he radically reversed course, unilaterally withdrawing the US from the JCPOA and reimposing Obama-era sanctions in a “maximum pressure” campaign. Trump executed the withdrawal despite verified Iranian compliance and fierce protests from European allies, claiming the deal was fundamentally flawed because its constraints were time-limited, ignored Iran’s ballistic missile program, and failed to address its regional proxy network. Though lacking international support, the “maximum pressure” campaign effectively crippled the Iranian economy once more, as global businesses chose to abandon Iran rather than risk US secondary sanctions.

Trump, however, went further than Obama. In January 2020, Trump escalated the confrontation by using military force, assassinating a top Iranian commander, General Qasem Soleimani, in a drone strike. Washington justified the assassination by claiming Soleimani had orchestrated proxy attacks on US assets in Iraq and was planning imminent future operations. However, the proxy groups denied responsibility, and the intelligence underpinning the “imminent threat” justification remains highly disputed.

The Biden administration's interim tenure marginally cooled open hostilities. While Biden avoided direct military strikes, he left the core “maximum pressure” architecture intact, prompting Iran to systematically step up its nuclear enrichment activities in open defiance.

In his second term, Trump re-escalated confrontations with Tehran well before the Hormuz crisis. Opting once again for direct military force, the administration launched Operation Midnight Hammer on June 22, 2025, an aerial bombardment of nuclear infrastructure at Natanz, Fordow, and Isfahan following the expiration of a 60-day US ultimatum to halt enrichment. This intervention served as the American component of the “Twelve-Day War”, which began on June 13 when Israel launched strikes against Iranian nuclear scientists and military command centres. While a ceasefire was brokered on June 24, 2025, it proved to be a fragile pause that held only until the far larger escalation of Operation Fury in February 2026.

From Washington’s perspective, its logic toward Iran is rooted in a post-Cold War ambition to preserve absolute hegemony over West Asia. This strategic posture is designed to protect the flow of Persian Gulf oil to global markets, protect Israel’s military supremacy, and prevent any local rival from dominating the region. Because the American policymakers refuse to view Iran as a legitimate or rational actor, Washington has systematically declined to accommodate Tehran’s core national interest in a “grand bargain”. Instead, its underlying objective has consistently tended toward “regime change”. Ultimately, the US views Iran as a dangerous disruptor of the West Asian status quo, a key state sponsor of terrorism, and an existential threat to American allies, particularly Israel and Saudi Arabia.

Conversely, while portrayed by adversaries as purely fanatical, Iran’s foreign policy is rooted in rational, defensive, and realpolitik calculations. Tehran’s core priorities are regime survival and sovereign independence, desires deeply shaped by decades of foreign subversion and the collective trauma of the 1980-1988 Iran-Iraq war. Its “Forward Defence” doctrine represents an asymmetric, pragmatic strategy designed to fight enemies outside Iranian borders, establishing a strategic buffer to prevent the US and Israel’s direct invasion of the homeland. Similarly, its funding and logistical support of political factions and militias resisting the US or Israeli presence is a calculated method of operationalising this external defence ring.

With the tactical cooperation of groups within the “Axis of Resistance” such as Hezbollah and Hamas, Iran has successfully created a formidable deterrent that drastically raises the cost of any conventional attack on Iranian soil. Its heavy investments in asymmetric assets, such as ballistic missiles, drones, and naval swarming tactics, are practical measures to compensate for severe conventional military weakness and international isolation. Ultimately, Tehran’s nuclear program serves as a strategic lever, designed to deter foreign aggression and force Washington to recognise the Islamic Republic as a permanent regional power.

The Trump Anomaly and The Israel Lobby

Traversing the history of US-Iran relations, it is evident that prior to the Trump presidency, successive US administrations since the 1990s avoided direct military escalation. They consistently limited their interventions to economic sanctions and proxy warfare, despite a permanently hostile diplomatic baseline.

What changed with Trump? The official reason provided for Operation Midnight Hammer, the 2025 aerial campaign bombing Iran’s nuclear infrastructure, was that Tehran was only weeks away from weaponising a nuclear device. However, the US Department of Defence concurrently assessed that the Iranian nuclear program has been set back by at least two years. This projected setback, paired with reports from Omani intermediaries indicating that Iran was willing to stop uranium stockpiling and permit full IAEA verification, severely undermined Trump’s rationale for the February 2026 offensive.

Because Iran’s nuclear and conventional military threat profile had not fundmentally shifted since the Biden administration, Trump’s pivot to direct military action uniquely isolates him from his predecessors. Highlighting this inconsistency, Trump has since stated that he is indifferent to Iran's enriched uranium stockpiles, openly contradicting the primary rationale his own administration cited to initiate the conflict.

Trump has long branded himself as an opponent of America’s “forever wars”, claiming to prioritise domestic security, rejecting the need to spread democracy in other regions, and demanding that regional allies defend their own backyard rather than rely unconditionally on Washington. These isolationist positions are explicitly codified in his administration’s National Security Strategy and the National Defence Strategy. In fact, the documents reflect some anxiety over the economic fallout of a hostile power seizing the Strait of Hormuz, a strategic vulnerability that should have logically deterred an attack on Iran. Trump’s decision to strike nonetheless underscores a reckless, unpredictable approach to foreign policy that diverges sharply from previous leadership; President Obama, for instance, intentionally delayed sanctioning Iran’s central bank for years specifically to avoid catastrophic oil shocks.

Rather than intervening directly in West Asia, Trump could have pursued a strategy of offshore balancing, delegating regional security responsibilities to regional allies. Adopting a less hostile stance and working pragmatically with Iran would have secured US interests far more effectively, as realists like Walt and Mearsheimer argue.

This aggressive willingness to deploy military force points to other domestic variables. Walt has noted that the outsized influence of the pro-Israel lobby played a decisive role in tipping the scales towards war. This domestic pressure was explicitly visible when Secretary of State Marco Rubio justified the strikes on Iran as a necessary measure to pre-empt Tehran’s retaliation against US regional assets following a unilateral Israeli bombing campaign.

Ultimately, Iran poses far more of a security concern to Israel than it does to the United States. Since 1979, the Islamic Republic has treated the Palestinian struggle as a core element of its foreign policy, championing and financing the armed resistance. Furthermore, Israeli leadership operates under the conviction that Iran seeks its physical destruction, a belief frequently anchored in a poorly translated comment by former Iranian President Mahmoud Ahmadinejad, who noted that the Israeli regime “must disappear from the page of time”, a phrase which he later clarified referred to an internal systemic collapse rather than through external military invasion.

A nuclear-capable Iran would fundamentally upend the balance of power, ending Israel’s regional hegemony and nuclear monopoly in West Asia, while severely constraining its unhindered genocidal tendencies against its neighbours. Furthermore, Iran’s logistical and financial architecture sustaining groups like Hezbollah in Lebanon, alongside Hamas and Palestinian Islamic Jihad in Gaza, has consistently thwarted Israeli strategic designs. Destroying Iran’s military capabilities is therefore seen by Israeli planners as a mandatory step to destroy the missile umbrella and advanced weaponry supply chains protecting and sustaining these proxy groups.

Israel and its domestic American lobby have a documented history of disrupting diplomatic engagement between Washington and Tehran, consistently steering US policy toward confrontation through sanctions and military threats. During the Clinton era, lobby pressure successfully influenced executive orders blocking US energy firms from investing in Iran. Under George W. Bush, the lobby aggressively pushed to keep military strikes on the table. This systemic intervention peaked in 2015 when Prime Minister Benjamin Netanyahu bypassed the White House entirely to address a joint session of Congress in a failed, yet highly disruptive, attempt to derail President Obama’s Iran nuclear deal. This influence extends beyond Iran; the lobby successfully campaigned for the 2003 invasion of Iraq, insulated Israel from US diplomatic pressure over its occupation of Palestine, and secured unconditional American material support during both the 2006 and 2026 Lebanon wars.

While Trump is by no means the first US President susceptible to this leverage, his administration stands apart due to the unprecedented concentration of hardline pro-Israel figures within his inner circle. Key West Asia envoys and negotiators in the recently collapsed nuclear talks, such as Steve Witkoff and Jared Kushner, are staunch supporters of Israel. Secretary of State Marco Rubio has built his legislative career as an aggressive defender of the US-Israel special relationship, consistently ranking among the top recipients of pro-Israel campaign contributions. White House Chief of Staff Susie Wiles previously consulted on Netanyahu’s 2020 reelection campaign. Trump himself has openly acknowledged his own political debt, singling out Miriam Adelson for praise in his October 2025 address to the Knesset, where he mused that her love for Israel might surpass that of the United States.

Concurrently, a lack of institutional pushback from the Democratic Party and their reluctance to criticise Israel for initiating hostilities can be explained by their own reliance on wealthy pro-Israel donor networks. As Walt and Mearsheimer observed, absent the structural distortions introduced by this lobby, US foreign policy would look radically different; Washington would be free to pursue an independent strategy aligned with its true national interest, including a balanced grand bargain with Iran. The persistent failure to secure such an arrangement has led directly to the current maritime blockade of the Strait of Hormuz, igniting a global energy crisis that now threatens macroeconomic stability worldwide, including in Malaysia. Given that this is not the first global oil shock to challenge the Malaysian state, it is critical to evaluate the nation's historical policy choices to understand why it remains fundamentally vulnerable to these external geopolitical disruptions.

Assessing Malaysia’s Energy Resilience

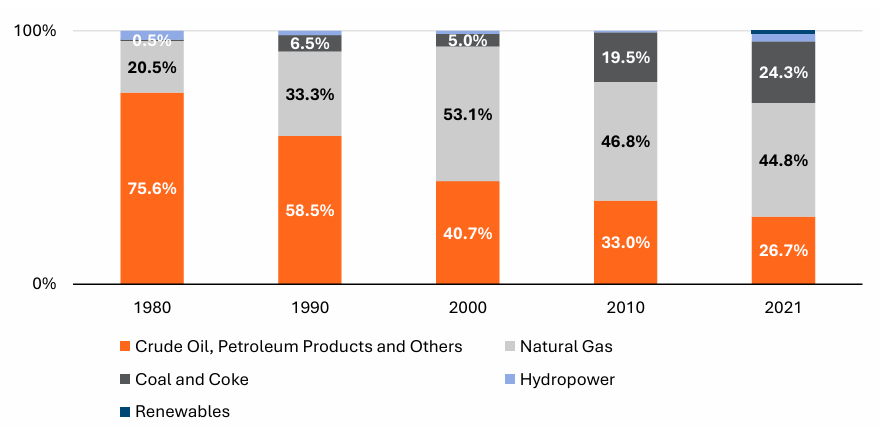

Approximately 40% of Malaysia’s crude needs are supplied by countries whose supplies must pass through the Strait of Hormuz. The risk of sudden energy supply shocks in this part of the world was not lost on past policymakers. Several policies in the past were crafted to reduce the country’s vulnerability, including the 1981 four-fuel diversification policy and the 2001 five-fuel diversification policy. By diversifying the type or source, alternatives may compensate for shortages during supply disruptions. The 1981 four-fuel policy targeted oil dependency following the 1970s energy shocks. By 2001, this was extended to a five-fuel policy, introducing renewables, especially from the palm oil and timber industries, to utilise industrial byproducts that would otherwise go to waste. Further policies to encourage the adoption of renewables were also intended to diversify the energy supply and reduce reliance on fossil fuels.

Chart 1: Malaysia’s Primary Energy Supply by Fuel Type, Percentage of Total, 1980-2021, Selected Years

Table 1: Herfindahl-Hirshman Index for Energy Concentration, Selected Years

* Data for Slovakia is for 2022

These interventions, however, have only shown partial success. While the primary energy data demonstrates a structural decline in Malaysia’s absolute reliance on oil (Chart 1), the true trajectory of this transition is best captured by the Herfindahl-Hirschman Index (HHI) for energy concentration (Table 1). Malaysia’s HHI score dropped from 0.457 in 1990 to 0.332 in 2021. Under this index, a score approaching zero represents a perfectly diversified energy supply, whereas a score of 1.0 signifies absolute reliance on a single fuel source. For perspective, Slovakia – a global benchmark for successful diversification – achieved a HHI of 0.205 in 2022, underscoring that Malaysia’s mix remains highly concentrated.

Although Malaysia has successfully diversified, this has mainly taken the form of increased reliance on natural gas and coal, which is still hydrocarbon-based, rather than on renewables, despite several policies to promote them since 2006. This is primarily because renewables, especially solar, have become cost-competitive with more established sources of energy only in the past few years. According to BloombergNEF, in Malaysia, standalone solar PV became cost-competitive with new combined-cycle gas turbines in 2018, whereas solar with a battery energy storage system (BESS) is expected to be so in 2026.

Nevertheless, Malaysia could have achieved a more rapid build-out, as Spain has demonstrated. Between 2019 and 2024, Spain's solar contribution rose from 5.6% of electricity generation in 2019 to 20.9% by 2024, increasing from 15.1 TWh to 58.6 TWh. For comparison, Malaysia’s solar share rose only to 2.1% from 0.8%, or from 1.46 TWh to 4.12 TWh, in the same period. This is partly due to Spain’s natural solar advantage, with a capacity factor of 18% to 24%, compared to Malaysia’s 14% to 16%.

However, the divergence is fundamentally institutional. Spain’s boom was unlocked after the 2018 repeal of the “sun tax”, which is a restrictive policy enacted in 2015 to counter legacy feed-in tariff deficits that had burdened the state budget. Following the repeal, Spain transitioned to a liberalised, open energy market, where developers are permitted to sell directly to end users via corporate Power Purchase Agreements (PPAs). This allows for rapid capital deployment, higher risk-adjusted return potential, and massive private-sector participation. Malaysia’s main solar build-out, on the other hand, relies on highly structured, government-led programs, such as auctions under the Large-Scale Solar (LSS) program, which started in 2016 and concluded its most recent round in September 2025. Although it offers lower risk and stability, it limits the explosive growth seen in fully privatised markets as government capital allocation for such projects is limited. Since late 2024, though, Malaysia has allowed corporates to source solar energy from the open market, permitting them to enter PPAs directly under the Corporate Renewable Energy Supply Scheme (CRESS). However, the timeline between this policy change and the start of the Iran-US war was too short to significantly alter the country’s energy supply composition, even if the policy proved effective.

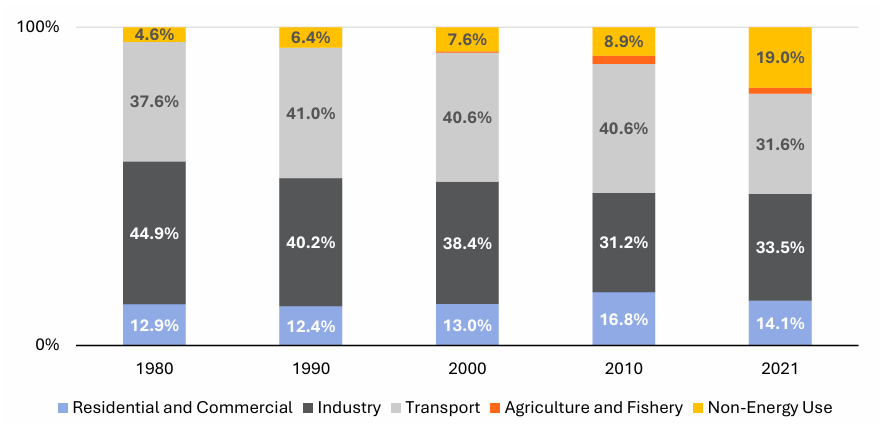

Chart 2: Malaysia’s Final Energy Demand by Sector, Percentage of Total, 1980-2021, Selected Years

Furthermore, success is more evident in diversifying the supply side than in the final demand side (Chart 2). This lack of success on the final demand side stems from the heavy energy use for transport and the country’s heavy reliance on private transport. In 2020, Malaysia had 535 cars registered per 1000 people, second in Asia only to Japan, which had 612 cars registered per 1000 people. According to the Minister of Transport, the country’s public transport modal share is around 20%, meaning the remaining 80% relies on private vehicles. These private vehicles are mainly powered by petrol, even as EVs are becoming ascendant: 81.1% of cars sold in 2025 were petrol-powered.

Malaysia’s heavy reliance on private transport is primarily due to inadequate and delayed investment in urban mass rail systems and the lack of political will to restrict the influx of private vehicles into city centres, especially in cities like Kuala Lumpur and Penang. While the government encouraged the development of bus networks and minibuses in the 1970s, the growth became haphazard, and the government phased out minibuses between 1994 and 1998. Around the same period, they also forced the merger of stage bus companies first into two, then into a single company, to streamline services. However, the new system failed to match the capacity and frequency of the old minibuses. In 1984, plans to introduce the LRT in Kuala Lumpur were shelved due to the global economic crisis of the mid-1980s. The reintroduced privatised LRT in the mid-1990s also faced financial difficulties following the Asian Financial Crisis, which affected its operational scope, forcing the monorail route length to be cut in half. Problems with integrating the LRT stations developed by the different private concessionaires also contributed to the poor user experience and incentivised private vehicle use.

Severe institutional fragmentation also contributed to poor integration among service providers, where at one time, responsibility for policies and approvals was divided among up to 12 ministries and various local agencies. Additionally, the government was reluctant to impose demand management policies on private vehicles, such as Area Road Pricing, which would have encouraged the use of public transport. Even though such plans were discussed as early as 1984, they were unpopular with the business community and the increasingly affluent middle class.

This structural failure is underscored by historical trends: between 1970 and 1980, Malaysia's public transit modal share fell from 37% to 33% despite expanding bus networks. Furthermore, the successful retention of a 50% public transit modal share in automotive-producing capitals like Tokyo and Seoul demonstrates that the core issue is not the national car industry itself, but rather a persistent deficiency in transit infrastructure quality. Following the government’s development of mass rapid transit (MRT) rail and the extension of the LRT line in the 2010s, public transport modal share began to increase again to 20% by 2025 from a low of 10–12% in 2008/2009.

Given the high reliance on privately owned motor vehicles, one way to mitigate the impact of international oil shocks is to diversify the energy sources used by private vehicles. Malaysia is one of the fortunate countries in the world to have oil and gas reserves large enough for export production. While Malaysia used to be a net oil exporter, it is now a net oil importer, though it remains a net exporter of petroleum products due to its substantial gas reserves. Powering a significant portion of vehicles with locally sourced gas would thus reduce our dependence on imported oil, as was attempted from the 1980s until recently. The NGV initiative strongly focused on public transport, beginning with the conversion of taxi cabs. The government took several steps to encourage the adoption of NGVs. They built NGV refuelling stations in urban areas, reaching 178 at their peak in 2013, encouraged the installation of tanks and conversion kits through tax incentives, and subsidised compressed natural gas to keep its price below 50% of the premium-grade petrol price.

Despite these efforts, NGV demand began to decline in 2015 due to inadequate refuelling infrastructure, high installation costs, and complex periodic safety inspections for gas tanks. At its peak, approximately 77,000 NGVs were on the road, representing less than 1% of registered vehicles. In late 2024, the Ministry of Transport announced that the retail supply of natural gas and the licensing of NGVs would be phased out completely by July 1, 2025, citing significant public risk, as vehicles modified between 1995 and 2014 have tanks reaching the end of their lifespans. Given the recent energy crisis, consumers might rue the recent move, as their continued availability would have provided a more affordable alternative to buying EVs as a mitigation strategy. At less than RM10,000, NGV conversion kits offered a low-barrier alternative for energy diversification. In contrast, the EV transition carries a significantly higher entry cost, with the cheapest models priced in the high tens of thousands, potentially excluding the very demographic most affected by oil price volatility.

Furthermore, with local reserves expected to last for at least ten more years, access to supply would be assured in the near term, even though to keep it affordable the government would have to sell it at below-market price. With oil, we have trouble finding replacement supplies, as we are experiencing now, since Malaysia is not 100% self-sufficient. However, even if the government were to backpedal on phasing out NGV, their ability to keep natural gas prices low has now been hampered. Previously, the government did not need to finance the lower gas price through direct subsidies, as Petronas, a federally owned, self-sufficient supplier, could directly set the domestic price, even at a loss, since it could still make money from gas exports from the Sarawak and Sabah fields. However, with Petronas’s role as the monopoly gas integrator broken by Petros, it is unlikely that Petronas would be willing to set prices below cost and take losses, as they could not profit as much from the Sarawak fields.

For diesel engines, Malaysia’s vast palm oil production could have served as an alternative fuel source during international supply shocks. Malaysia has policies to promote biofuel production through the National Biofuel Policy of 2006, while the Malaysian Biofuel Industry Act of 2007 mandates the government to prescribe specific biofuel chemistry and blending volumes. Although the government introduced policies to encourage a reduction in dependency on fossil fuels, these policies primarily serve as a price-stabilisation mechanism for the plantation sector rather than a strategic buffer against international energy volatility. It seemed more focused on its second objective: ensuring economic returns to stakeholders through guaranteed demand, especially during periods of low crude palm oil prices.

Given the focus, there is no ready reserve of palm oil biodiesel that the government could immediately access during the present oil shock. It is a ‘drop-in’ solution that alters the present composition of diesel production rather than building stocks. The government initially mandated a 5% blend of palm oil-derived fatty-acid methyl esters with regular petroleum diesel for the transport sector, increasing it to 10% in 2018, 15% by June of this year, and eventually to 30% for heavy vehicles by 2030. Given that biodiesel is sold as a blend that still primarily relies on petroleum diesel, this will limit its mitigatory role in reducing reliance on fossil fuels, unless the biofuel portion becomes the majority or no longer needs to be blended with petroleum diesel entirely.

Furthermore, unlike NGV previously, which was fully supplied by a self-sufficient, federally owned monopoly supplier, biodiesel producers are mostly private companies not controlled by the government. This means producers are likely to have a weaker social agenda and will want to sell biodiesel at the prevailing market price to maximise profits. The federal government cannot control the price of biodiesel at the pump through direct price-setting and will therefore need to resort to direct subsidies. Given that the need to review our energy sources also arises to contain a bloated fuel subsidy, the need to further subsidise makes the option less attractive except during periods where oil prices are above crude palm oil (CPO).

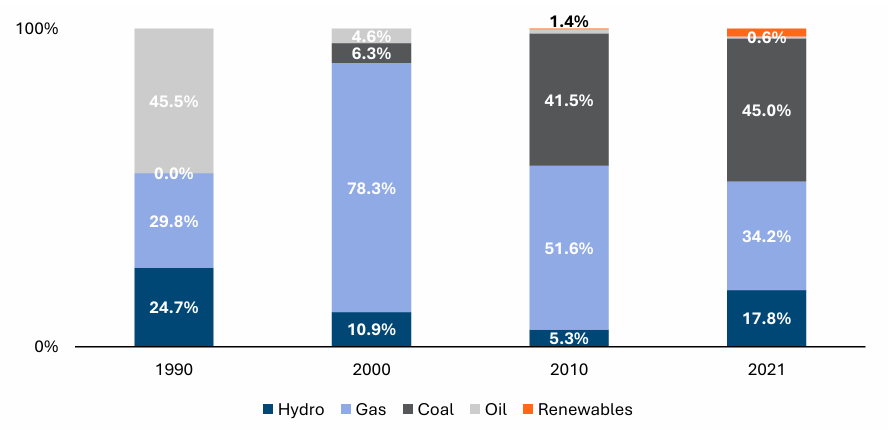

Chart 3: Malaysia’s Electricity Generation Mix, Percentage of Total, 1990-2021, Selected Years

Apart from preparing existing vehicles to have access to alternative fuels, another mitigation strategy that could have been pursued was accelerating the transition to electric vehicles. Since EVs are powered by electricity, their ability to mitigate energy shocks depends on the electricity provider's diversification strategy, pushing responsibility upstream (Chart 3), unless one can generate electricity themselves, such as through solar PVs. However, as mentioned above, this is more expensive than retrofitting existing vehicles to use alternative fuels and may alienate lower-income groups. The government indeed provided incentives for EVs, such as exemptions from import and excise duties for completely built-up cars, though the window is closing, and tax relief for EV charging installation. These incentives have encouraged the adoption of EVs.

However, the RM100,000 floor price limit for CBU imports has discouraged those looking for a lower price range and a more extensive EV transition. Furthermore, EVs only became more affordable circa 2022–2023, when tax incentives were introduced and Chinese automakers began offering desirable, affordable models. Given this narrow developmental window, the market share of electric vehicles has not scaled rapidly enough to offset the current crisis, even if cheaper models were allowed to be imported, since average consumer vehicle replacement cycles span six to eight years. As such, even if the government had provided more incentives prior to the crisis, such as allowing the import of cars priced below RM100,000, this would not have significantly mitigated the country’s oil dependency.

Conclusion

While Malaysia could not have done anything to prevent the war between the US and Iran, past policy choices have dictated how exposed the nation remains to such external shocks. Although various political and economic drivers shaped these historical choices, a distinct common thread explains why the state failed to build deeper reliance on renewables and public transit. Some of this weakness stems from untimely policy reversals; primarily, however, past administrations prioritised short-term fiscal restraint to avoid expanding the national deficit. Beyond broader industrialisation goals, this mindset explains why the government chose to pursue a national automotive project to expand mobility rather than invest in urban rail transit as early as possible. This automotive strategy relied primarily on private finance through sales to domestic consumers insulated within a protected market. Though requiring an initial state investment and low energy costs, the national oil subsidy bill at the time remained negligible.

Likewise, expanding highway infrastructure to facilitate mass motorisation relied on privatisation models rather than direct state outlays. While this logic was fiscally expedient when global crude prices were low—with fuel subsidies averaging a marginal 0.4% of government expenditure throughout the 1990s—it ultimately became a structural trap. Today, with petrol and diesel heavily subsidised to shield consumers, the fiscal burden has exceeded historical levels. The subsidy bill consumed 14.3% of total government expenditure in 2022 at RM42 billion, and the Treasury's current projection of RM58.4 billion under this oil shock highlights how politically and financially paralysing these blanket mechanisms have become.

Had past administrations been less averse to expanding public expenditure to build comprehensive urban rail networks and utility-scale renewable capacity, the country would be far less vulnerable to external supply shocks. Furthermore, any ongoing state funding required to maintain public transit pales in comparison to the multi-billion ringgit hemorrhaging currently witnessed at the retail pump. Ultimately, Malaysia’s current predicament serves as a stark warning for future policymaking. When a government refuses to invest in the structural capital required for energy independence, it will inevitably find itself paying a far higher premium to subsidise its own vulnerability.

.png)

.jpg)

%20(1).jpg)