Introduction

As we witness the US-Israel attack on Iran and the war unfolding, the Trump Administration continues to pursue trade policies that may be deemed illegal under US domestic law. Recently, the Supreme Court of the US (SCOTUS) has deemed that the US Reciprocal Tariffs (also known as Trump Tariffs) are illegal. The Trump Administration has yet to develop a mechanism for US importers to receive refunds for tariffs paid before the SCOTUS decision. Revenue raised from these tariffs is estimated at USD189.4bn1.

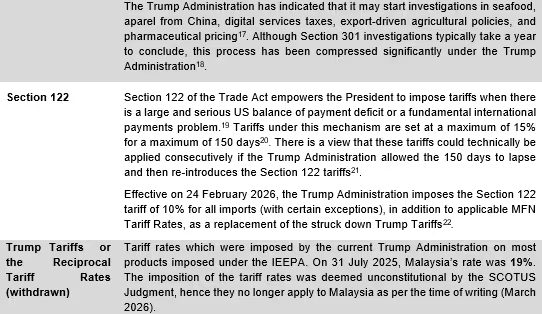

The Trump Tariffs were declared unconstitutional by SCOTUS on 20 February 2026 (SCOTUS Judgment)2. These tariffs were imposed based on the International Emergency Economic Powers Act (IEEPA). Immediately after the judgment was issued, the US announced another policy tool – Section 122 of the 1974 US Trade Act (Trade Act) – to impose a tariff of 10% to replace the Trump Tariffs3. This rate is on top of the pre-Trump Administration tariff rate that is applicable to all its trading partners.

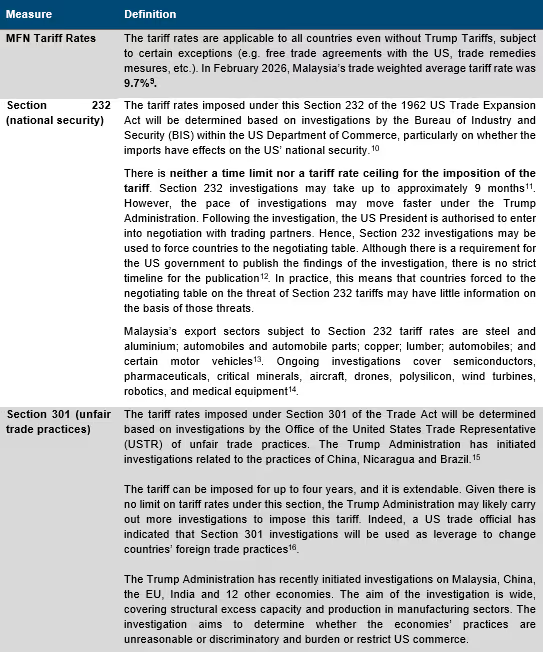

There are four key policy tools that the Trump Administration can use to impose tariffs. These policy tools are known as Section 122, Section 301, Section 232 and the pre-Trump Administration tariff rate (known as the Most-favoured Nation (MFN) Tariff Rates). Among the existing policy tools, Section 232 and Section 301 are seen to be the more durable policy tools, while the Section 122 tariffs are being challenged in US domestic courts4. Although Section 122 tariffs apply to most goods, they are limited to a maximum 15% tariff rate. This is lower compared to Section 232 tariffs that have been applied at 50% tariff rates.

This article aims to highlight the policy tools that the Trump Administration are most likely to use this year. Further, this article explores the SCOTUS Judgement and its impact on the US-Malaysia trade deal that was signed in October 20255. This article is intended for educational purposes only and should not be considered as legal advice.

Stacked Tariffs: Understanding the Multi-faceted Approach of the Trump Administration

In essence, the effective tariff rate that is applicable to Malaysian products entering the US is made up of multiple policy tools that are ‘stacked’ on top of each other. This stacking mechanism, peculiar to the Trump Administration’s tariff policy, requires US importers to track the tariff rate imposed by each policy tool on a specific good. For example, in the semiconductor industry, a large number of semiconductor products were exempted from the Trump Tariffs. This was because the Trump Administration has been conducting a Section 232 investigation into the effects of semiconductor imports on the US’ national security since April 20256. In the past, the Trump Administration has imposed tariffs of up to 50% on steel and aluminium products following Section 232 investigations7.

As explained above, the US may use multiple policy tools to impose various tariffs, which may be ‘stackable’ (non-exhaustive) on Malaysian products entering the US. Understanding these different policy tools (see Table 1) is essential, given the imminent possibility of their use by the US, as evidenced by the imposition of Section 122 tariffs immediately after the SCOTUS Judgment declared the IEEPA tariffs unconstitutional. Recently, the US has also initiated investigations covering Malaysia under Section 301 with a broad aim to address structural excess capacity and production in manufacturing sectors, which are claimed to displace US domestic production or prevent investment and expansion in US manufacturing production8. These investigations cover Malaysia, China, the European Union (EU), India, and 12 other economies.

Table 1: The Various Tariffs that may be Applied by the US

SCOTUS Judgment Overview

The Trump Tariffs have been challenged in the US domestic courts. The Trump Tariffs which were imposed under the IEEPA, in particular, were deemed unconstitutional by the SCOTUS because the IEEPA does not grant the President with the authority to impose tariffs. In fact, prior to Trump, no other US President had ever used the IEEPA to impose tariffs.

In its judgment, the SCOTUS explained that the US Constitution grants the Congress with the authority over taxes and tariffs. The words ‘regulate’ and ‘importation’ in the IEEPA are considered ambigious, thus cannot be interpreted as delegation of the authority from the Congress to the President to collect taxes or tariffs. Such delegation of authority to impose tariffs must be done expressly and with certain restrictions. Lawsuits have been filed for the refund, and the Court of Appeals for the Federal Circuit allowed the request for them to continue at the US Court of International Trade23.

SCOTUS Judgment’s Implications to Previously Charged Trump Tariffs

The Trump Tariffs continued to be imposed on various countries (including Malaysia) until the issuance of the SCOTUS Judgment on 20 February 2026. Accordingly, one legitimately questions the possibility of obtaining refunds for the unlawful tariffs which have been collected by the government throughout the period. Recently on 4 March 2026, the US Court of International Trade ordered the US Customs and Border Protection to refund all IEEPA duties that have been collected24. In this regard, Malaysian exporters that have been charged with the Trump Tariffs should also monitor for such refunds, although the process for refunds remains unclear due to the complex logistics that would need to be established25.

SCOTUS Judgment’s Implications to the Malaysia-US Trade Deal

The Trump Tariffs form a part of the deal reached in the Agreement between the United States of America and Malaysia on Reciprocal Trade (ART), whereby many Malaysian exports are charged with a tariff rate of 19% on top of the MFN tariff rates, with certain exemptions26. The ART expressly refers to the Executive Orders which further refer to the IEEPA as the basis for the imposition of the Trump Tariffs. Accordingly, with the SCOTUS Judgment, the Trump Tariffs become unlawful and hence the agreed tariff rate under the ART is no longer applicable. Nevertheless, given that tariff issues were only one aspect of the deals agreed in the ART, the other deals remain applicable.

It is noteworthy that the ART will only be fully enforceable 60 days after both countries have ratified the agreement. The SCOTUS Judgment may present an opportunity to rebalance the ART and renegotiate the agreement's terms, given the primary benefit of reduced Trump Tariffs no longer exists. Malaysia’s Minister of Investment, Trade and Industry has confirmed that the ART has not been ratified by the government,27 hence it has not entered into force yet and there may still be room to renegotiate its terms. As explained above, with the lower additional tariff of 10% imposed under Section 122 to all countries, any renegotiation should target for lower tariff or other more favourable terms.

Conclusion

Tariffs imposed on Malaysia’s exports to the US should be understood as part of a phenomenon known as ‘tariff stacking’, where multiple types of tariffs may apply to the same product. While the Trump Tariffs (which forms one of the primary benefits for Malaysia under the ART) have been declared unconstitutional, the Trump Administration has imposed a replacement tariff of 10% under Section 122. In addition, ongoing investigations in the US may lead to further tariffs on specific sectors of Malaysian exports. Thus, Malaysian exporters need to be aware of how ‘tariff stacking’ is applied for each product and the sectors that may face additional tariffs in the future.

Given the SCOTUS Judgment has resulted in a more favourable tariff rate for Malaysian products compared to the tariff rates negotiated under the ART, this presents an opportunity for Malaysia to rebalance the ART and renegotiate the agreement's terms in light of the disappearing tariff rate benefits under the ART.