.jpg)

Introduction

The past few years has seen an unprecedented sequence of global crises. Malaysian’s firms and households have not fully recovered from the aftermaths of Covid-19 and the Ukraine War, and yet here we are again, faced with another crisis; - the blockade of the Straits of Hormuz.

How do we approach a strategy of remedial measures to the current energy crisis? Do we respond with knee-jerk measures, or do we see an opportunity to take a more measured approach for the longer term to ensure greater resilience and sustainability in the future? And it is also important to ask what kind of principles and values should guide this transition.

This Views article will attempt to structure the discussion of by asking two basic questions: -

1) How does the energy crisis affect our economy and our sense of economic security and well-being? What is our ‘working baseline’?

2) What is the response to our baseline?

In attempting to answer these 2 basic questions, the structure of the economy is analysed within 3 periodic phases; namely Phase 1- the commodity-based economy; Phase 2- the export-orientated manufacturing economy, and Phase 3- the diversification and emerging services economy. The role of the State in coordinating the economy with differing priorities and political orientation within these periods are briefly explained.

A description of the current state of the households and firms is presented as the current ‘working baseline’. Short-term measures to combat the ill-effects of the energy crisis is critical, but this article suggests that it should be viewed as a continuum to build resilience through approaches of long-term structural interventions in the economy. As economic growth positively affects the character of the society as a whole, some discussion of the principles that ought to underwrite these approaches are also presented.

As a final note, this is the first essay of a series of articles discussing this critical topic. In the coming weeks, KRI will be producing more articles on the different ways and means in which we can articulate responses and policy considerations.

Preamble

Traditionally, the role of the State has primarily been for the provision of defence, securing public order, the prevention of epidemics and an aversion towards mass discontent. Since the end of World War 2, the peace endured by countries created the luxury of social expenditure as the main budgetary responsibility of these modern states, especially those espousing social democracies. These spending initiatives initiated, for example, the New Deal in the USA, Scandinavian social democracies and Britain’s welfare state. Malaya in 1957, was to a certain extent, infused by the ideologies of the West due to colonial occupation; especially in the ways that the colonial experience established the institutional arrangement within the corresponding ideologies.

The post-independence years and through to the formation of Malaysia was shaped by a worldview focussed on improving life chances, generous medical and educational services, optimistic prospects of upward social mobility and perhaps above all – an undefinable but ubiquitous sense of security. The post-war baby boomers knew of a world for improving life chances, and the state is the provider of such opportunities. Despite having radically different religious, cultural and to some degree political beliefs in a highly ethnicised environment, nevertheless there were concerted effort to develop a common platform based on government programmes with the objectives of justice, equal opportunity, and economic security.

Since the mid-1980s, Malaysia has undergone considerable liberalization and deregulation. These movements were seen to go against earlier initiatives first introduced in the early 1970s, where the state played a central role in determining the course of the economy. The early 1980s witnessed a paradigm shift in global economic thinking with the ascent of leaders such as Margaret Thatcher in the UK and Ronald Reagan in the US. This transformative phase, underscored by a re-evaluation of the State's role in delivering goods and services, propelled the propagation of neoliberalist tenets, advocating for reduced government intervention through fiscal austerity measures. Notably, Malaysia's response to this shifting paradigm was epitomised by the Malaysia Incorporated policy (Malaysia Inc.) in 1983.

Neo-liberalization and deregulation policies continued until the present to encourage trade, investment and new employment. The basic maxim is that economic growth ought to be steered by the private sector, with the State mainly serving as a facilitator. This was driven by an ongoing perception that market-led initiatives were intrinsically more efficient. On the other hand, government involvement was seen as an impediment in delivering goods and services efficiently.

In recent years, catastrophic epidemics and global economic meltdowns such as the sub-prime crisis, Covid-19, the Ukraine war and now the US/Israeli Iran war has tested the role of the State in providing economic and social security for its citizens. This is within the backdrop that the government’s sphere of influence in the workings of the economy has been declining markedly.

Structuring the Discourse

Global distresses appear to have been recurring more frequently than before. Far from recovering the aftermath of Covid-19, the Ukraine War affected many of our trading goods and domestic firms, and now the blockade of the Straits of Hormuz threatens a new energy crisis, since ‘old’ energy (as opposed to green energies) is the backbone of developing economies. In terms of scale of the supply of energy, it is estimated that approximately 1/5 of the world’s crude oil and liquified natural gas (LNG) passes through the Straits. Moreover, other petrochemicals supplies (for example ethylene, methanol) that are foundational for other products (amongst others; plastics, synthetic rubber, building materials) are disrupted as well.

There are many prescriptions on what needs to be done to buffer our country from the political, socio-economic shocks depending on which discipline one belongs to. However, this would depend on what aims and outcomes expected from such initiation. This would then be subject to how the nature of the problem(s) are defined. Economists would categorize these disruptions as supply side shocks; the political scientist explicating the geo-political effects of the fracturing American hegemony and the rise of China on the country’s selection of trading partners, and not least the social theorist postulates on the possibility of returning to a society of collectives in weathering financial shocks rather than relying on the impulses of a heavily financialised economy.

Even though the subject is highly complex and multidimensional, it might be prudent to structure our responses by asking 2 basic questions:

1) How does the energy crisis affect our economy and our economic sense of security and well-being? What is our working baseline?

2) What is the response to our baseline? Do we respond with reactive measures, or do we see this as an opportunity to develop a more realistic appraisal of how states in the developing world ought to respond to potential future crisis? And perhaps more fundamentally what are the principles that should underwrite this transition?

Question 1: How does the energy crisis affect our economy and our economic sense of security and well-being? What is our baseline?

The economy and the labour market

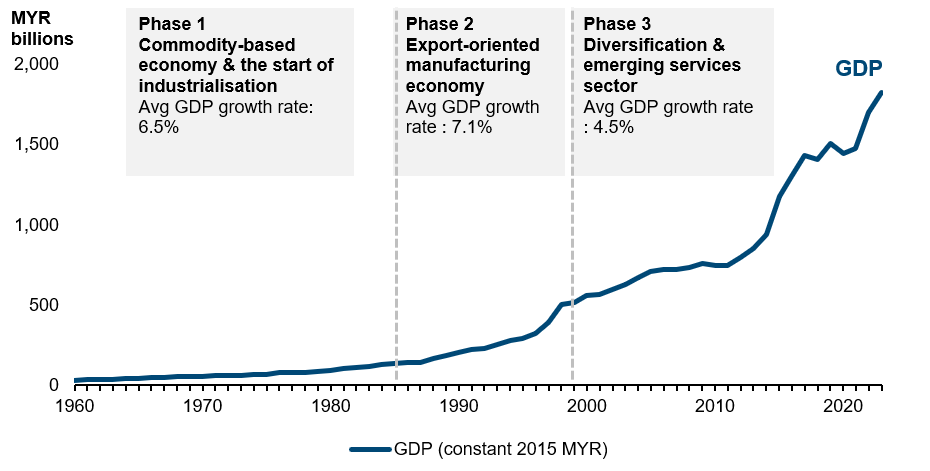

It is important to understand the structure of our economy as it has evolved over time and the types of employment created over the years. Malaysia has witnessed rapid economic growth, where real GDP at 2015 prices grew 34-fold from Ringgit Malaysia (RM) 39 billion in 1960 to 1.3 trillion in 2020, as shown in Figure 1: Real GDP and the three phases or economic transformation and diversification, 1960 - 2023. The growth could be explained within three periods of economic transformation and diversification: Phase 1- the commodity-based economy; Phase 2- the export-orientated manufacturing economy; and Phase 3- the diversification and emerging services economy. Average GDP growth was 6.5 percent, 7.1 percent, and 4.5 percent, respectively.

Figure 1: Real GDP and the three phases of economic transformation and diversification, 1960 – 2023

The 3 phases of development created the share of employment as seen in Figure 2: Share of employment by sector.

Figure 2: Share of employment by sector, 1982 – 2022

Figure 2 depicts the share of employment within the services sector (modern and non-modern) has grown significantly over the preceding decades, mirroring somewhat period 3 of the country’s growth trajectory -i.e. the diversification of the economy and the emergence of the services sector. Non-modern service is divided into two categories: traditional and social services. Traditional services include wholesale & retail, transportation & storage; admin & support services; accommodation & food; other services. Social services cover education, health & social work, public administration, defense & compulsory social services, and utility services. Alternatively, modern services are further categorized into finance & insurance, real estate, information & communication, professional, scientific & technical (DOSM, 2024)

The transition from agriculture to the services sector has increased the GDP threefold but it is however, accompanied with major disappointments. Malaysia’s economy depicts the classic though vicious cycle of low-wage, low-profit, and low-productivity trap, rendering it as a cheap labour model of business and economic growth. Most SMEs and large manufacturing firms still operate within traditional cost-driven concerns and the preoccupation for low overheads leading to a downward spiral of hiring low-skilled workers with low wages, and the resistance to invest in innovation. Moreover, most SMEs utilise unskilled foreign labour as they are seen to be cheap, widely available, and highly flexible in satisfying the needs of smaller firms, without taking into consideration the detrimental effects of taking this route such as short termism, stunting the growth of the economy and real wages.

This has suppressed any possibility of alleviating the problem of underemployment and fair wages for the labour market. The problem is particularly acute for the bottom 70 percent of Malaysian’s household population who struggle to make ends meet, due to the inability of household incomes to cover the rising costs of living (KRI; 2019, 2024). Bank Negara (2025) reported perilous instances of wage stagnation from 2010-19, where the absolute increase in the annual real wage per worker was approximately RM56 for the bottom 50 percent of the wage distribution. Moreover, MOF stated that between 2019 and 2020, there was a decline in graduates earning above RM2,000 by 2.3 percent, while those earning below the minimum wage grew from 48.8 percent to 51.1 percent. Policy interventions are now concentrated on median wage, not just at the minimum wage, to ensure significant improvements in the wage outcomes of the labour market.

The distribution of labour in the economy suggests limited demand for high-skilled workers. The proportion of firms investing in R&D is negligible, and a significant amount of the retained profits has been distributed to shareholders' dividends rather than being invested back into the business, or as returns to labour. Consequently, the compensation of employees' share of income to GDP for Malaysia in 2024 was 33.6 percent, relatively lower regionally (Singapore 37.8 percent, Philippines 34.6 percent), and even worst-off compared to advanced economies (UK 49.8 percent and Germany 54.7 percent) (Bank Negara, 2025). An economy that does not compensate its workers sufficiently will face problems attracting high-skilled workers (World Bank, 2010). This is just the basic nature of economies.

Trade Openness

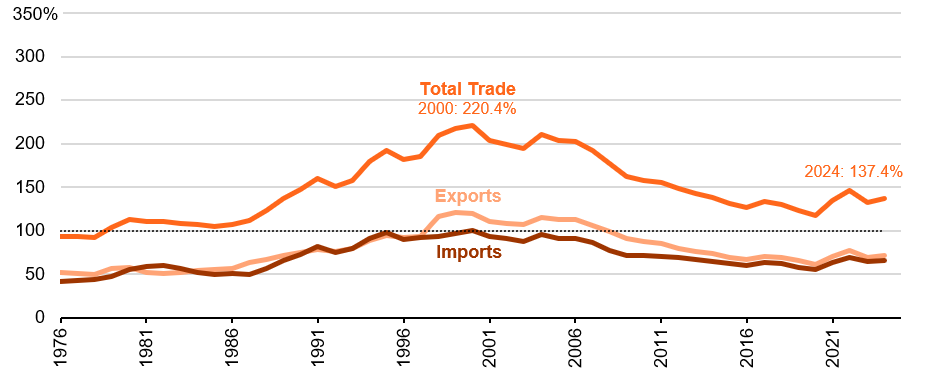

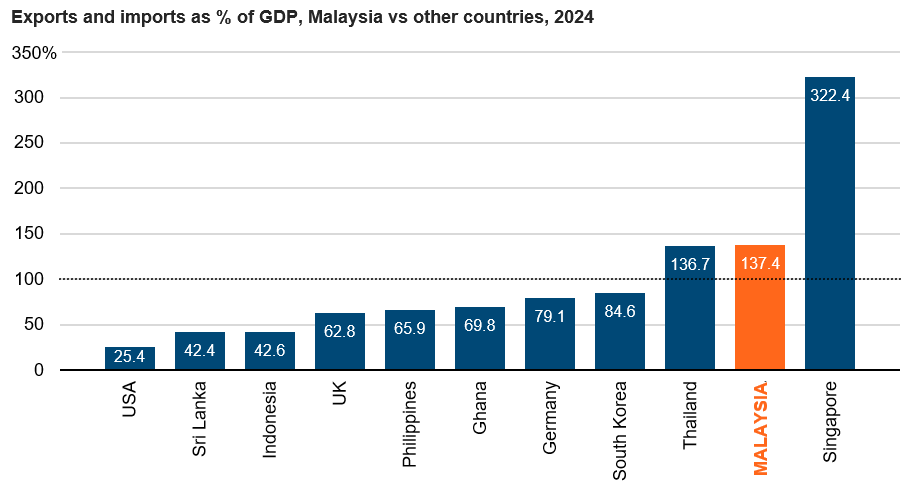

Notwithstanding the structure of the economy, Malaysia trades with many countries, as can be seen by the two figures below. Malaysia’s total trade in 2024 is 137.3 percent of its GDP (Figure 3) showing nation that trades quite extensively as compared to other countries (Figure 4).

Figure 3: Exports and imports as % of GDP, Malaysia, 1976 – 2024

The Working Baseline

An economy that practices trade openness will be inevitably affected by any distortions in the supply of fuel, which is exacerbated when countries are scrambling to secure access to sufficient energy and other fuel-related by-products themselves. Moreover, when our trade imports and exports exceed the value of our GDP, our ability to function as a thriving economy would be seriously impeded when the costs of international logistics exceed certain break-even thresholds. There will be supply shocks to imported immediate goods that we consume as households, as well as intermediate goods that firms use as part of being in the global value-chain of production.

Furthermore, in a labour market outcome where nearly 70% of households are struggling to make ends meet and already require fuel subsidies and cash transfers under normal circumstances, mainly reflects the severity of inadequate wages to maintain a decent standard of living. This should serve as our working baseline.

In what way is this made manifest? For now, the reaction has been uneven because of the time lag for the adverse effects to come in. For example, some sectors (agriculture, fisheries) that depend on diesel for their daily operations have requested for more government assistance. If these firms experience an increase in their costs of production, then this will be passed on to households. Can these price increments be absorbed? For the bottom 70% of households- the answer is most likely no.

Question 2: What is the response to our baseline? Do we counter with reactive measures, or do we see this as an opportunity to develop a more realistic appraisal of how states in the developing world ought to respond to potential future crisis? What are the principles that should underwrite this transition?

Perhaps it is prudent to ask what led to the Malaysian economy to its current condition of low wages, low productivity and minimal investment in R&D? Was it the cumulative effects of the political-economic priorities we made? It is also important to bear in mind that the role of the state in managing the economy has been arguably in gradual decline since the mid-80s. And as a matter of consequence what we are witnessing now are presumably outcomes of a largely private-led economy. Therefore, when the energy crisis shocks the economy, to what degree this has compromised the State’s ability to provide effective countermeasures?

Approaches to the responses

Apart from responding with measures to alleviate the struggles of both firms and households in the short and medium term, global economic shocks give us alternative perspectives and opportunities to strengthen our economy in the long term. This is the transition needed to be a more resilient economy; when firms themselves invest in the structural reforms required to improve their respective companies’ innovative capabilities. Some firms might argue that investment in better technologies will only diminish their profits because the costs of innovation will be funded by retained profits and external loans. Additionally, firms and shareholders might already be satisfied with the current level of profits. However, when firms are disrupted by external economic shocks, it is clear only those who possess better capabilities and technologies will have a better chance for survival. Therefore, investing in technological improvements not only increases the resilience and survival of firms, but it will also create more opportunities for sustained increased profit in the future.

Reinert (2007) reminds most developing countries to draw lessons from actual practices and activities of developed nations in their process of economic growth as opposed to the kind of advice they often give. This is because in the arena of global trade, a significant proportion of FDIs invested in less developed nations are of firms that are experiencing decreasing returns to scale in their own country. This simply mean the costs per unit of production has gone up, due to say rising wages or the costs of doing business has increased. Therefore, their strategy is to migrate or friend-shore at countries (mostly in less developed countries) where the factors of production- i.e. land and labour- are relatively cheaper so that these firms can continue to experience increasing returns to scale again. The mid-1980’s manufacturing initiative brought these types of FDIs, ostensibly portrayed as being able to deliver the positive impact of the multiplier effect to the industry. Though it worked to a degree, the medium to long-term benefits are debatable, especially in terms of wage growth and real productivity gains. Unfortunately, most developing states believe this is the method to attract FDIs or MNCs, by offering a least-cost business model. In actuality, it is a ‘race-to-the-bottom’ type of ‘competition’ because the only competitive advantage it develops is low and even lower wages.

It must be understood that between the finished products and raw materials lies the real and sustainable multiplier effect; i.e.an industrial process demanding and creating new knowledge, mechanization, technology, division of labour and increasing returns to scale with employment for the masses. Good economic sense suggests not to continuously supply the world with raw materials because it will lead to over production and a rapid fall in domestic wages. Producers of raw materials inhabit a world of ‘perfect competition’ that forces producers to give their productivity increases to their customers in the form of lower prices. Only in ‘imperfect markets’ do firms experience increasing returns to scale. Factors that are present in rich countries are ‘imperfect competition’, synergies between economic sectors, economies of scale and scope, and the presence of economic activities which makes these factors possible- because economic growth is activity specific, it can take place in some economic activities but not in others.

An increasing acute problem for the past several decades has been the continuing stagnating of wages. It takes place in certain economic context but not in others. For example, Nobel laurate Edmund Phelps argues for the American case after the US subprime crisis “ For me, a compelling hypothesis is that workers, shaken by the 2008 financial crisis and the deep recession that resulted, have grown afraid to demand promotions or to search for better-paying employers-despite the ease of finding work in the recent tight labour market. A corollary hypothesis is that employers, disturbed by the extremely low growth of productivity, especially in the past ten years, have grown leery of granting pay rises- despite the return of demand to pre-crisis proportions (2 Nov 2017, Project Syndicate)”.

In addition, the low levels of unionization around the world and the spread of globalization have decreased workers’ bargaining power as has the rise of monopsony power. Workers are afraid that their employers will move to say Vietnam or subcontract their work to India if they request for better wages and working conditions. The surge in number of workers entering the market without high job absorption rate has also created a ‘race-to-the-bottom’ type of competitive advantage in terms of low wages. Many are willing to enter the job market with lower wages rather than be unemployed. In essence, it might not just the level of unemployment in the country, but also the behaviour and decision-making of workers and firms that created stagnating wages. Consequently, increasing wages will not necessarily be inflationary, as touted by many employers. This makes the initiative for progressive wages and living wages important, not just to cover the living expenses but to retain talent in the country.

The values that inform us

The quest for economic growth should not be an end in itself. Growth ought to be subordinate to the kind of society that we want to create, nurture and sustain. This means that growth should be the enabler that allows the values we deem important to flourish. A fundamental mistake in many developing countries is to sometimes see growth, especially economic growth and wealth as a key indicator of progress without linking it to broader questions of ethics, shared values and the well-being of society at large.

The prevailing conditions of trade and commerce in a given country, (be it during good or bad economic times) relied upon approaches rooted in cultural traditions and landscapes where virtues, social norms and trust are encouraged in economic exchanges (Hirshman, 1977). Under such social and political conditions, firms tend to behave more responsibly; supported by a communal intuitional arrangement, for the betterment of society. As society gave firms the opportunity to trade and prosper, this opportunity in turn created a sense of moral obligation for firm owners to behave responsibly. This ethos is very much needed in our country.

The role of public policy to nudge firms to behave well is very relevant. This is because market-led economic activities can sometimes systematically produce more for example, pollution and congestion, than beneficial outcomes like better wages or on-the-job training. Due to the fact that economic growth positively affects the character of the society as a whole- and crucially, because neither openness nor democracy is a good that private markets trade and price- there is a consequent role for policy measures to seek growth beyond what the market would provide on its own.

Conclusion

Crises offer the opportunity for reflecting on our country’s baseline and understanding the limitations and opportunities we can afford ourselves. We draw lessons from experiences of other countries, and our own historically, in detangling the web of developmental initiatives and the impact it has had. Then we can devise a strategy that is suitable to our context and objectives.