Introduction

Malaysia has a high level of digital adoption that has facilitated strong growth in the use of financial technologies (fintech) such as digital payments. The Central Bank of Malaysia (Bank Negara Malaysia, BNM) has instituted an Interoperable Credit Transfer Framework (ICTF) that fosters innovation and the development of other fintech services, such as digital banks and cross-border digital payments.

With the intention of expanding Malaysia’s participation in global finance and digital trade, both public and private entities in Malaysia are exploring international partnerships for cross-border digital payments. This could improve Malaysia’s economic growth and expand its role in the global economy.

When considering global digital finance, there are at least four policy issues to take into account, namely digital financial inclusion, increasing risks of financial cybercrime, disruptive effects of unregulated decentralised finance and cryptocurrency, and geopolitical considerations.

In a four-part series on Malaysia’s expanding fintech and digital payments space, I assess the growth and current state of Malaysia’s digital adoption and use of the internet for financial transactions and consider opportunities and initiatives in fintech, particularly in terms of crossborder digital payments. This is a fast-moving and fast-growing sector rapidly introducing innovations and new technologies to consumers.

The first article presents an overview of Malaysia’s digital adoption and use of fintech, focusing on the growth in digital payments from 2011–2024.

This second article in the series reviews the contribution of BNM’s ICTF and the introduction of digital banks to Malaysia’s financial services landscape.

The third article explores the demand for and developments in cross-border digital payments between Malaysia and other countries.

The fourth article discusses policy considerations around the use of digital payments and fintech in a globalised society.

BNM’s Interoperable Credit Transfer Framework (ICTF)

In 2019, BNM introduced the Interoperable Credit Transfer Framework (ICTF)1 to enable credit transfer services between banks and non-bank e-money issuers. This approach was instrumental in facilitating a more streamlined digital payments infrastructure in the country and has broad implications for any large-scale digital systems infrastructure, from electronic health records to government database architecture.

The ICTF required financial institutions, e.g. banks, to participate in the shared payment infrastructure. This meant that bank account holders could now transfer funds across banks digitally, without having to withdraw physical cash or write cheques. Benefits of this interoperability included convenience for retail banking customers, added security for small businesses that did not need to carry around large sums of cash for bill payments, and ease of accounting by means of a more efficient audit trail.

The ICTF also included customer protection measures such as instant notifications and transfer limits to protect users from fraud. Instant notifications are intended to alert a user immediately when any transaction is made or received, while transfer limits are supposed to cap the amount and frequency of any given transaction. These measures notwithstanding, the number of fraud and scams have continued to increase over time.

The introduction of the ICTF may have been one of the factors that led to the consolidation of the e-wallet landscape. When e-money was first introduced, merchants had to partner with each ewallet provider individually and display the relevant QR code for customers to scan in order to enable e-money transactions. It was common to see five or more QR codes laid out in a shop for customers to scan using their preferred e-wallet app.

Under the ICTF, BNM required Payments Network Malaysia Sdn Bhd (PayNet), Malaysia’s shared payment infrastructure provider, to set up an interoperable QR (“quick response”) standard. This common QR standard, known as DuitNow QR, has become the default QR code used for digital payments across Malaysia. These days, merchants are more likely to display just one or two QR codes for customers to scan.

Although there are 482 non-bank e-money issuers licensed by BNM at the time of writing, observations suggest that there are not that many e-money apps in popular use. Most banked customers tend to use their banking apps for digital payments. Unbanked consumers may also be likely to use popular superapps, such as Grab and Touch ‘n Go to access multiple digital services, including digital payments.

At the time of writing, DuitNow transaction fees for consumers have been waived for transactions up to MYR5,000. There is a MYR0.50 fee for transactions above MYR5,000 which banks have waived for individual users. There is also a transaction fee for businesses, which has been waived for micro, small and medium enterprises (MSMEs)3. This makes the DuitNow QR a preferred and accessible digital payments option for small businesses that normally are disinclined to accept credit card payments due to merchant fees.

Licensing of five digital banks

As Malaysia’s digital economy develops, the push for financial inclusion continues. Digital banks are an effort to make banking easier for unbanked and underbanked groups, especially where physical branches of banks are unavailable. Digital banks provide all the retail banking services of brick-and-mortar banks without the need to be physically present at a bank branch. All processes, from account registration and e-KYC (electronic Know Your Customer, i.e. a digital means of identity verification) to credit risk assessments, are done digitally, usually using a smartphone.

On the one hand, digital banks may be able to offer lower fees or better promotions as they do not have to contend with high operating expenses. On the other hand, customer service and support may be a challenge without a physical location and human resources.

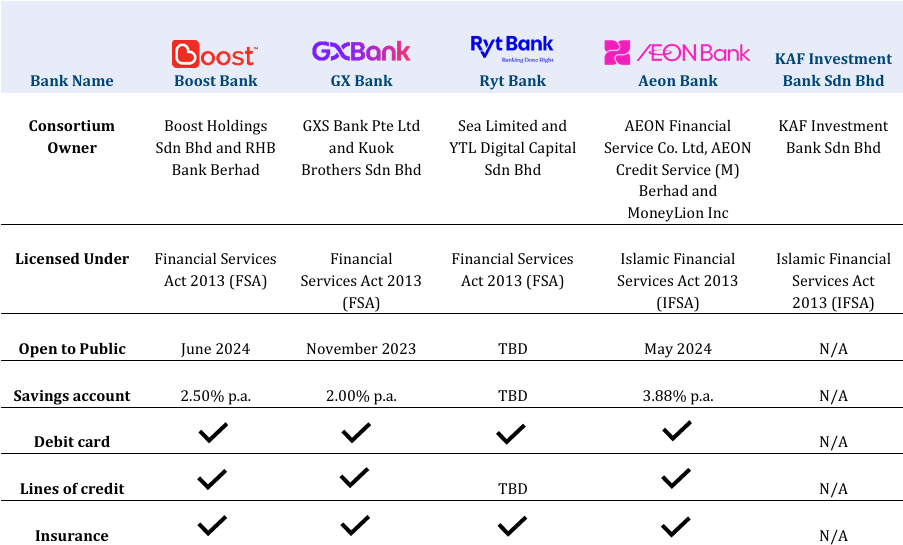

BNM released a licensing framework for digital banks4 in 2020 and, after considering 29 applications, awarded licenses to five digital banks in 20225, summarised in Table 1. These five digital banks were then required to go through a period of operational readiness testing, subject to audit and validation by BNM. At the time of writing, three of the five banks are open to the public.

Table 1: Summary of licensed digital banks in Malaysia, as at February 2025

It is not yet clear whether the introduction of these digital banks has successfully enabled greater financial inclusion. BNM’s Financial Inclusion Framework 2023–20266 suggests that 96% of adults have an active deposit account. However, it is also common for an individual to have multiple bank accounts, suggesting that this statistic is overestimated.

The Financial Inclusion Framework also highlights that “79% of Malaysian adults used digital payments, of which 42% did so for the first time after the [Covid-19] pandemic7” (p4). Digital banks may become an avenue for the unbanked and underbanked to open their first bank account. Conversely, digital banks may simply be another banking option for those who already have multiple bank accounts.

Detailed statistics from BNM, for example, on the number of new digital bank accounts in underserved communities or among the previously unbanked, can shed light on whom digital banks are primarily serving. As at December 2024, BNM reports that the three digital banks open to the public received RM2.3 billion in deposits from 1.3 million customers, 60% of whom are in underserved areas8. Further research on the share of deposits and the take up of different digital financial services would be useful to assess financial inclusion.

Conclusion

One of BNM’s primary objectives is to promote financial inclusion to support sustainable socioeconomic development. Two contributions that BNM has made towards financial inclusion are the introduction of the Interoperable Credit Transfer Framework (ICTF) and the licensing of five digital banks. The ICTF has paved the way for financial inclusion in digital payments and the broader fintech ecosystem by enabling cross-platform transactions across financial institutions, businesses and consumers within a shared digital payments infrastructure. However, it remains to be seen how effective digital banks will be at enabling financial inclusion among underbanked and unbanked populations, especially those living in rural areas. Aggregated statistics suggest a growing consumer base among underserved groups while anecdotal evidence suggests they remain an urban-centric financial tool serving the already-banked. Future research on the take-up of digital financial services is needed to assess progress in Malaysia’s financial inclusion efforts.

_2.avif)