Introduction

For decades, night markets have served generations of Malaysians in ways that go beyond what meets the eye. More than a sociocultural heritage, night markets carry dual functions: they are both socioeconomic institutions that sustain livelihoods and food infrastructures that serve consumers of various backgrounds. In Kuala Lumpur (KL) alone, thousands of hawkers depend on night markets as their source of income1. Street food, including those sourced from night markets, contributes 13% to 50% of daily energy intake among individuals in developing countries2. Despite this dual significance, night markets and those within the ecosystem are typically invisible in official statistics and remain inadequately understood.

Night markets today are facing multiple challenges that threaten their long-term viability. Alongside the persistent vulnerabilities inherent to the informal and precarious nature of hawking, night markets face growing competition with urban spaces and modern retail. The sustainability of night markets matters not only for the hawkers who rely on them for a living, but also for the communities they serve, especially lower-income families, who depend on them as an accessible source of food. Yet, in the absence of evidence base, attempts to close the gap between policy intent and lived realities remain limited.

Efforts to address any problem must begin with an understanding of the context. Hence, KRI conducted a survey between September 2025 and October 2025 to characterise night market hawkers and consumers as well as to understand their perceptions and experiences. A total of 894 hawkers and 769 consumers across 32 selected night markets in KL were interviewed, contributing to a rich dataset on an understudied sector.

In light of the ongoing Iran war and its potentially far-reaching implications for small businesses and households, this article presents preliminary findings from the survey to shed light on the vulnerabilities and needs within the night market ecosystem. This article intends to inform targeted mitigating measures to alleviate the cascading impacts of the crisis on night market communities. The following discussion is organised into two parts: the first part examines the vulnerabilities of night market hawkers, while the second provides insights into the food security significance and concerns of night markets to consumers.

Night Markets as Lifelines: Hawker Dependence and Vulnerability

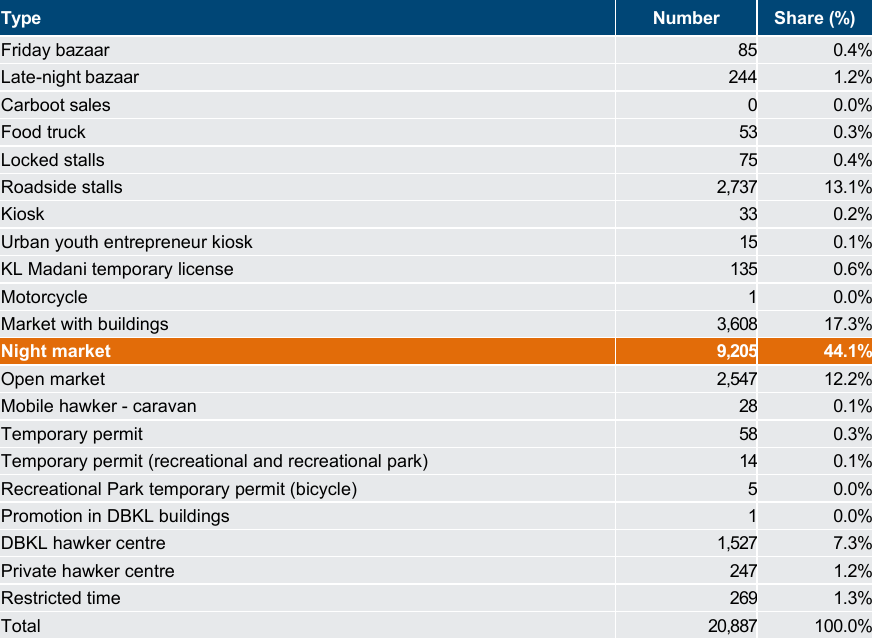

Night markets represent a sizeable informal economy in Malaysia. Statistics from the Kuala Lumpur City Hall (DBKL) show that as of 2025, the sector accounted for 44.1% of the total informal businesses in KL, the largest share among all types of licenses3 (Table 1). Although this does not necessarily reflect the distribution of hawkers across other states, the sizeable presence of night market businesses in KL suggests that these markets serve as an important means of livelihood for hawkers, particularly in urban areas where night markets tend to be more established. Historically, the growing number of hawkers in the city was driven by several factors, including rapid urbanisation and supportive government policies such as more liberal issuance of traders’ permits and licenses, wider access to loans and improvements in infrastructure, as discussed further in our previous discussion paper4.

Table 1: Number and share of active hawker licenses, by category of business in KL, 2025.

Furthermore, our survey findings corroborate the sector’s critical role in providing employment opportunities. Over 80% of the surveyed hawkers employed at least one worker to help with their operations, with 64.5% employing one to two workers, while 21.9% employed three to four workers. This implies that hawkers themselves are also job providers, and those who work for them are also dependent on night markets to earn a living.

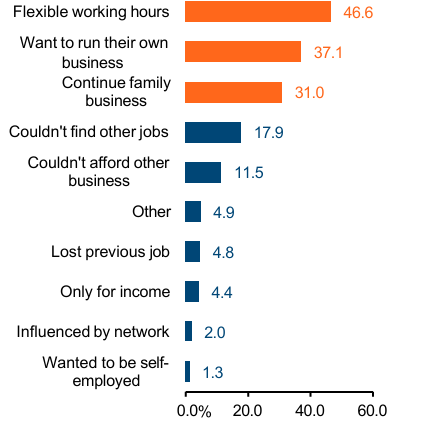

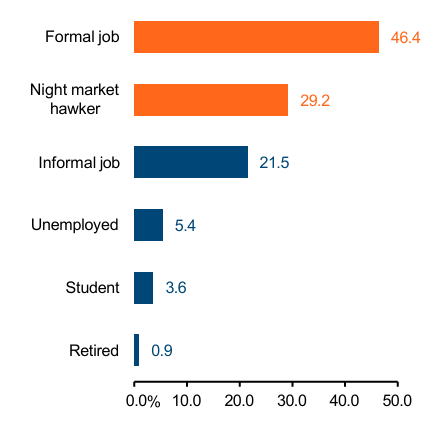

The significant size of the night market economy is also driven by several advantages offered to the hawkers when venturing into the sector, such as flexible working hours (46.6%), as well as opportunities for individuals to run their own business (37.1%) and family business (31%), as displayed in Figure 1. Moreover, our survey found that over 46.4% of the hawkers moved from formal employment to night market hawking, while 29.2% have long been night market hawkers (Figure 2). This implies that night market business may not be a mere temporary pursuit for most hawkers but rather their main choice or the only option for livelihood.

Figure 1: Share of hawkers by their motivation to join the night market sector.

1. Others include old age/retirement plans (n=5), for fun/socialisation/combatting boredom (n=5), to raise children (n=3), obtaining immediate salary (n=3), and due to health issues (n=1).

2. Respondents can choose more than 1 option, so percentages sum to more than 100%.

Figure 2: Share of hawkers by the type of their previous occupation.

Key Challenges Confronting Night Market Hawkers

Although night markets provide crucial livelihoods for hawkers and they have benefited from supportive government policies, they remain susceptible to several notable challenges. These include 1) lack of income security, 2) rising economic pressure and 3) lack of financial resilience and social safety nets.

Lack of Income Security

The informality of night markets inherently affects hawkers’ income stability as daily wage earners, especially in times of crises5. By informality, it is not only about hawkers being unlicensed, particularly when our findings show that 98.2% of the surveyed hawkers held licenses. Rather, it refers to the structural conditions of self-employment that involve fluctuations in earnings and the absence of employment benefits and job security.

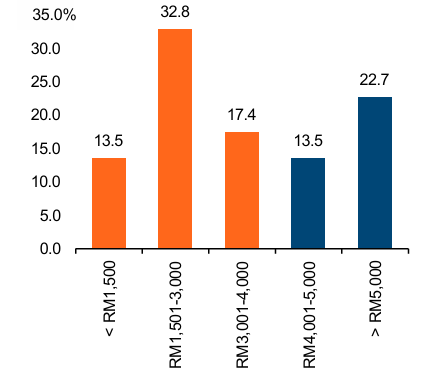

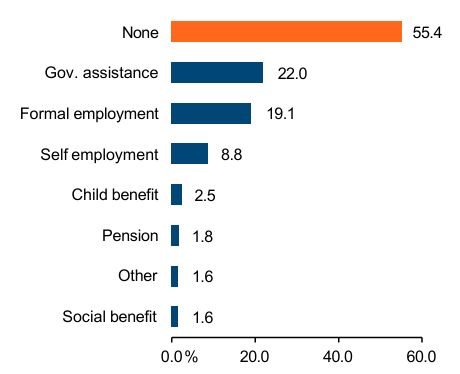

In this case, the circumstances for hawkers based on our survey appear concerning, as 63.7% or close to two-thirds of hawkers earned less than RM4,000 per month. This is notably lower than the national mean and median income levels at RM9,155 and RM7,017 in 2024, respectively6 (Figure 3). Furthermore, more than half of the hawkers relied solely on income from night markets, without government aid or other income sources to support their household needs (Figure 4). One-third or 34% of hawkers earned less than RM4,000 per month without any other income sources listed in Figure 4. A single income source dependency, coupled with low and unstable earnings, could result in substantial household-level financial stress for hawkers in the event of business disruptions.

Figure 3: Share of hawkers by reported average monthly net income range.

Figure 4: Share of hawkers by sources of additional household income.

Rising Economic Pressure

Even before the start of the Iran war, night market hawkers have been facing increasing economic pressures that have affected their ability to generate profit. Hawkers face rising costs of raw materials; about half of them experienced a cost increase between 10% and 39% over the past year at the time of the survey (Figure 5). Additionally, 28.6% of hawkers agreed that their businesses compete with retail stores or online delivery platforms; while this is not the majority, it still indicates that a significant proportion of hawkers face the combined effects of increased competition and higher raw material costs.

This is disadvantageous to night market hawkers through two mechanisms7: 1) increased costs of operation, without a corresponding price increase, decrease profits; and 2) increased competition forces hawkers to maintain or lower prices to remain competitive. The combination of these effects, as currently experienced by hawkers, decreases markups, profits and, therefore, income from both the cost and revenue perspectives.

Figure 5: Distribution of hawkers by perceived inflation rate for raw materials from Q4 2024 to Q4 2025.

Exacerbating matters, hawkers have yet to fully recover from the Covid-19 pandemic. Despite four years since Malaysia’s transition to an endemic phase of Covid-19 in April 20228, 69.6% of respondents reported sustained worsening of business performance compared to before the pandemic (Figure 6). When disaggregated by product categories, the overall sentiment of post-pandemic worsened performance is consistent. This frames the poor business environment in which hawkers operate: unrecovered from the last big shock while persistently facing challenges to their profit-generating capacity.

Figure 6: Distribution of hawkers by their perceived change in business performance compared to pre- pandemic.

Lack of Financial Resilience and Social Safety Nets

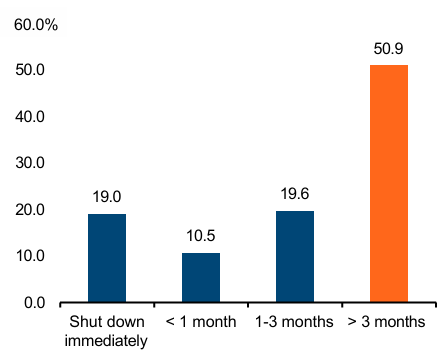

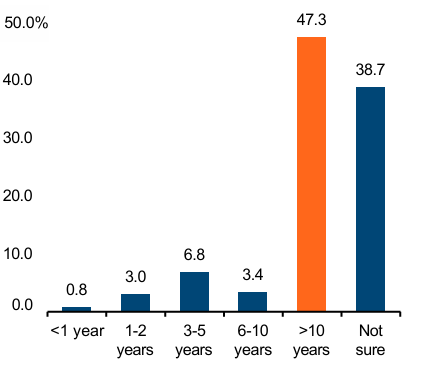

Despite sustained increases in economic pressures, many hawkers are hopeful about the sector's longevity and their ability to navigate its waters in times of trouble. Among the hawkers surveyed, 50.9% believed their businesses could continue operating for over three months, even when not making any profits (Figure 7). Furthermore, 47.3% of hawkers intended to continue operating their stall for over 10 years (Figure 8). However, a smaller but still significant proportion of hawkers appeared less resourced or unable to weather setbacks, with 29.5% reporting an inability to sustain their business beyond a month under no-profit conditions (Figure 7), and 19% would be forced to shut down immediately.

Figure 7: Share of hawkers by period of continued business operation under no-profit conditions.

Figure 8: Share of hawkers by duration of continuing to operate their stall.

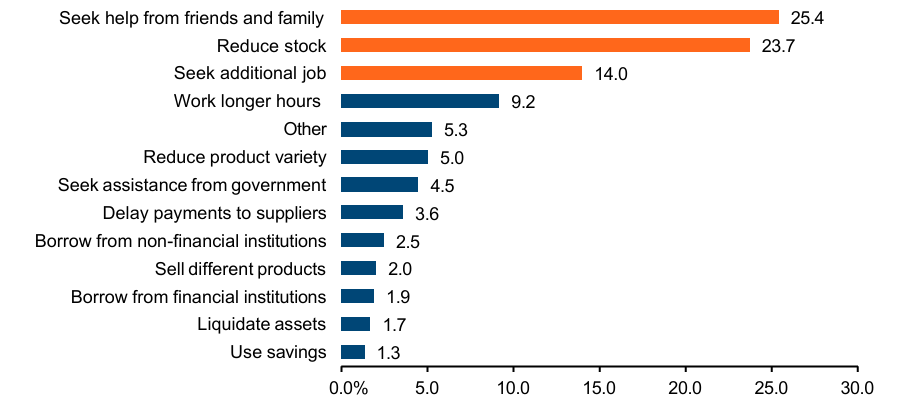

When asked about their first course of action during times of financial difficulty, 63.1% of hawkers stated either: 1) seeking help from friends and family, relying on their social safety net; 2) reducing stock, which is a form of business contraction; or 3) seeking an additional job, indicating labour substitution (Figure 9).

Figure 9: Share of hawkers by first course of action when facing financial difficulties.

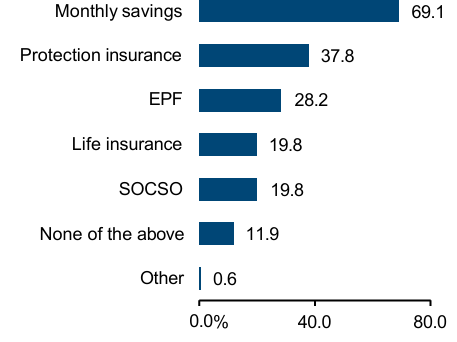

Additionally, many hawkers (69.1%) reported contributions to monthly savings, but the proportions of those who reported contributing to protection insurance (37.8%), Employees' Provident Fund or EPF (28.2%), life insurance (19.8%) and Social Security Organisation or SOCSO schemes (19.8%) remain low (Figure 10). Specifically, for social insurance and pension schemes like EPF and SOCSO, only 35% were covered. A lack of contribution to mechanisms that are designed to provide more reliable and sustainable protection for times of financial difficulty and retirement could imply that, through monthly savings alone, hawkers remain ill-prepared for such circumstances. Furthermore, despite having monthly savings, there is an overall reluctance or inability to be financially self-sufficient, without the need for business contraction or labour substitution, during times of financial difficulty, as seen by only 3% of hawkers choosing to first liquidate assets or use savings (Figure 9). This could indicate that, while many hawkers have personal savings, these amounts may be inadequate to form a viable financial safety net in times of difficulty.

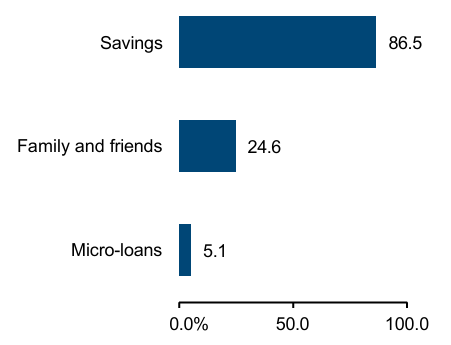

When faced with financial difficulties, only 1.9% would choose to borrow from financial institutions, while just 4.5% would try seeking assistance from the government (Figure 9). This low reliance on government assistance and formal credit is also reflected in their main sources of business capital (Figure 11), where 86.5% of hawkers tapped into their own savings and 24.6% relied on friends and family, consistent with a previous study9. In contrast, only 5.1% of hawkers accessed microloans, despite the availability of such schemes and the fact that most hawkers are licensed. This pattern could be caused by several factors, including limited access to formal credit for hawkers, low awareness among hawkers and difficulty in meeting financing requirements by loan-providing institutions10. Hence, understanding the factors contributing to this low uptake remains an important area for further enquiry.

So, while night market hawkers remain optimistic about their prospects in the sector, many do not possess the financial resilience to weather any shocks to their profit-making ability—a predicament that has only been exacerbated since COVID-19, driven by inflationary pressures and increased competition. Part of this vulnerability is likely due to a combination of factors— low uptake of formal sources of credit, limited savings and low social insurance and protection coverage.

Figure 10: Share of hawkers with monthly savings and social protection schemes.

1. Other includes Gold (n=2), unit trust/ASB (n=1), andTabung Haji (n=1).

2. Respondents can add more than 1 option, so percentages sum to more than 100%.

Figure 11: Share of hawkers by the main sources of capital for their business.

1. Responses for other categories are not included in the chart as the share is negligible. These include capital from government grants (n=13), religious bodies (n=7), cooperatives (n=3) and others (n=5).

2. Respondents can choose more than one option, so percentages sum to more than 100%.

Night Markets as Food Security Infrastructure

Food Security Significance of Night Markets

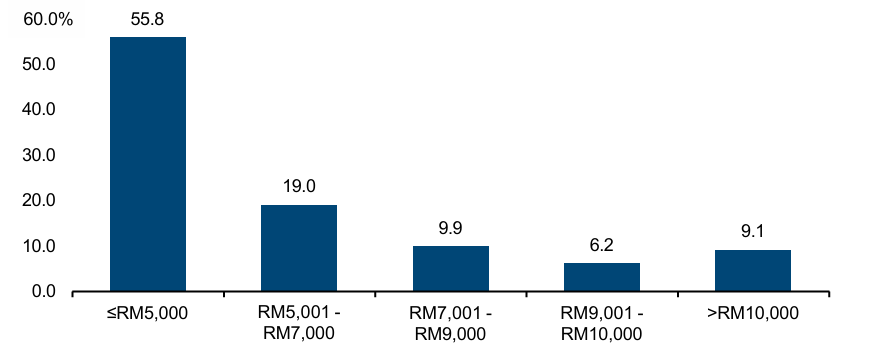

Night markets are not only important sources of livelihood for hawkers, but also serve as vital lifelines for surrounding communities by providing accessible and affordable food options, particularly for households and individuals with low incomes or at risk of food insecurity. Figure 12 showed that more than half (55.8%) of surveyed consumers belonged to the B40 income group, while another 35.1% came from middle-income households. Additionally, 21.6% of respondents, or one-fifth, reported concerns about not having enough food to eat, especially among those with unstable income sources, such as part-time workers, the self-employed, and the unemployed.

Figure 12: Share of consumer respondents by self-reported household income group.

Consumers mainly rely on night markets to access food. Our survey shows that more than half of consumer respondents (58.7%) visited night markets to purchase ready-to-eat food and beverages at least once a week, with a smaller proportion visiting for raw ingredient provisioning, such as fresh fruits, vegetables and meat. While night markets generally serve consumers of all backgrounds, their role as a food source is more significantly relied upon by the lower-income households. On average, nearly one in four (24.3%) consumers allocated at least one-fifth of their monthly food expenditure to night market foods, with a higher level of dependence among consumers with a household income below RM7,000 (Figure 13).

Figure 13: Share of consumers by the share of night market food spending out of total monthly food expenditure and income levels.

Proximity as a Key Driver of Night Market Patronage

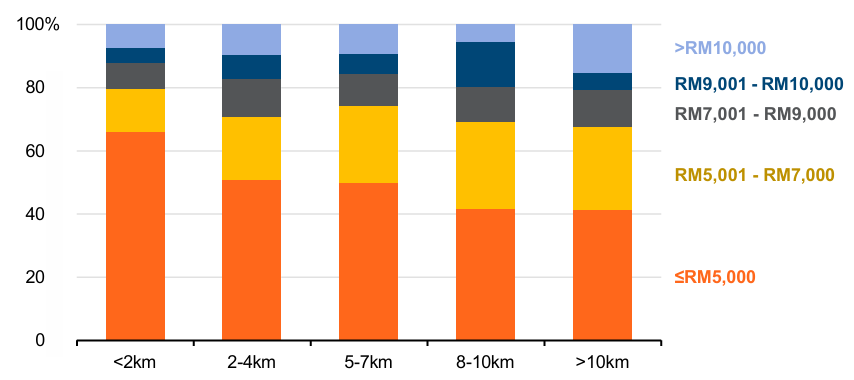

Having a night market in close proximity is key to driving patronage. Survey data show that consumers who lived closest to night markets were more likely to visit more frequently and tended to have lower incomes (Figure 14). There can be two interpretations to these findings: firstly, night market reliance is not only driven by affordability but also by physical accessibility. Secondly and more importantly, the proximity of night markets to those that they mainly cater to, the low-income population, suggests that night markets function as an informal food infrastructure strategically embedded within the community that needs them the most. This also means that the food behaviours of lower income households are more significantly shaped by the environments and choices they encounter at night markets, which they likely access within their constraints. Any disruptions to night market operations may, therefore, have negative impacts on food access, particularly for households without transport or fewer resources to explore other food sources.

Figure 14: Distribution of consumer respondents by proximity to night market and income level.

Gaps in Food Safety and Nutritional Quality

While night markets play an important role in urban food access, the survey findings also point to several concerns regarding the nutritional quality and safety of food sold in night markets. As more households rely on night markets for regular meals, questions about food quality become increasingly important from both public health and food security perspectives.

Food choices at night markets are abundant, but they are dominated by less healthy options. Based on the profiling of 811 food and beverage products sold at night markets, more than half (54.6%) were considered discretionary food, referring to food high in fat, salt and sugar with limited nutritional value. Mixed food accounted for the second-largest share (28.2%), mostly consisting of meals such as nasi lemak and mixed rice. In comparison, core food items, which consist of fresh, minimally processed and healthier options, represented only 17.1% of the assessed food items.

Beyond nutritional quality, the findings also highlight uneven food safety practices and infrastructural limitations at night markets. Although Malaysia has an established regulatory framework governing food hygiene and handling, survey responses suggest that hawkers’ experiences with food safety monitoring may vary by location and vendor. Around 80% of surveyed hawkers reported that food safety inspections rarely took place during their operations, while another 9.4% stated that they had never experienced inspections (Figure 15). Additionally, Figure 16 showed that 36.1% of the surveyed food vendors reported not attending mandatory food handling and hygiene training.

Figure 15: Share of hawkers by their perceived frequency of food safety inspection.

Figure 16: Distribution of hawkers by attendance in food handling and hygiene practice training.

Limited infrastructure may also affect food safety practices at night markets. The majority of surveyed hawkers (85%) brought their own water from home for use at night markets. Observations also found limited access to hygiene facilities, with only 6% of vendors having access to an individual sink. Overall, these findings highlight an important challenge within the night market ecosystem. While night markets continue to provide affordable, accessible food to urban communities, especially lower-income households, the surrounding food environment may also expose consumers to long-term nutritional and food safety risks.

Conclusion and Policy Recommendations

Preliminary findings reveal the interdependence between hawkers and consumers within the night market ecosystem. Consumers are key in driving the night market economy, directly contributing to hawkers’ livelihood. The vulnerabilities of hawkers, however, can have implications for night market stability and continuity, which are key for ensuring food access for consumers, particularly those from the lower income groups.

This interdependence becomes more important than ever during crisis. The current Iran energy crisis does not create vulnerabilities in night markets. Rather, it acts as a stress test exposing and deepening existing ones. As discussed earlier, our survey findings show that night market hawkers are generally lacking in income security and financial resilience, with one-third earning below RM4,000 per month as their only source of income and nearly two-thirds without any social insurance or pension schemes. Furthermore, most of them have not recovered from the negative impacts of the COVID-19 pandemic, which led to significant business declines, but are already facing another wave of economic pressure. These vulnerabilities can limit hawkers’ capacity to sustain operations and cause income loss in times of crisis. For lower income consumers who depend on night markets, disruptions to night market supply and operations are not temporary inconveniences but a risk to their food security.

Addressing these vulnerabilities will require deliberate long-term measures; however, reducing the extent to which the ongoing crisis exacerbates them is an urgent priority. To support them in navigating the rising cost of operations, maintaining hawker inclusion in the existing packaged cooking oil, liquefied petroleum gas (LPG) cylinders and BUDI MADANI diesel subsidy schemes is imperative, while ensuring the less-informed and resource-constrained hawkers can access these supports.

The low uptake of formal credit or government financial schemes, such as microloans, despite their availability, does not just signal the need for more targeted promotion and accessible enrolment support at night market sites. It also highlights the need to reassess application requirements and disbursement processes to better accommodate hawkers' needs and constraints. This is supported by previous studies that consistently showed that the lack of awareness was not the only barrier11. Behavioural and perception-related factors, such as debt aversion, lack of knowledge of application method, high upfront costs, ineligibility and the perception that benefits do not justify the time and effort required, were also commonly reported12. For hawkers with low incomes and small-scale operations, short-term cash assistance with low eligibility criteria may be more helpful in helping them manage immediate supply and price shocks.

Social insurance and pension schemes such as i-Saraan and Self-Employment Social Security Scheme (Lindung Kendiri) have long been available for informal workers, including night market hawkers, yet uptake remains low. The low participation is also in contrast to the implementation of mandatory participation in Self-Employed Social Security Schemes (SKSPS) for registered hawkers beginning January 202513. In times of economic difficulties, hawkers may be even less willing to set aside income for contributory schemes, even when coverage would matter most. To close the participation gap, a temporary increment of the special incentive, coupled with widespread outreach and on-the-ground sign-up mechanisms, can be considered. In the longer term, measures need to go beyond addressing the availability and accessibility gap to future-proof the system into one that meets the needs of the hawkers, through mechanisms such as default opt-in at the point of licensing.

Last but not least, existing food assistance or vouchers that are administered through e-wallets or digital payment channels, such as Sumbangan Asas Rahmah (SARA), can be expanded to include licensed night market stalls. The case for this is supported by the survey that found 91% of surveyed hawkers have already adopted e-wallet payments and 55.8% of night market consumers are from the low-income segment. This measure can deliver dual impacts—supporting the income generation of night market hawkers while ensuring food access for low-income or vulnerable consumers.

The COVID-19 pandemic demonstrated how prolonged economic shocks can leave lasting, and in some respects, irreversible impacts on the night market ecosystem. For many hawkers, post-pandemic recovery remains incomplete, further compounded by reduced footfall and a shift in consumer purchasing patterns towards digital trade. The current crisis, therefore, warrants timely and targeted interventions to prevent the existing vulnerabilities within the ecosystem from further deepening. Although the survey findings are limited to KL’s context, they offer a glimpse into the broader night market and hawker landscape in Malaysia—one that signals the need for greater attention and more concerted efforts to address the vulnerabilities faced by this group.

The preliminary findings presented here are part of an ongoing study on KL’s night markets. A final report containing more comprehensive findings, analysis and policy recommendations will be released upon completion of the study.

.jpg)