Introduction

We have heard the Strait of Hormuz pronounced open, nearly open, or ‘largely negotiated’ no fewer than six times since its closure in March 2026, and each time it wasn’t. This may have changed on 15 June 2026 when the US and Iran formally signed a memorandum of understanding to cease hostilities for at least 60 days and reopen the Straits of Hormuz1.

A delicate equilibrium has been struck between the US and Iran, which could hold or collapse, as they continue negotiations on major issues such as Iran’s nuclear programme and a permanent termination of military operations, including in Lebanon2. Iran has announced that commercial ships seeking to pass through the Straits of Hormuz now need to submit requests to a new agency, the Persian Gulf Strait Authority, with no fees charged for 60 days3.

It is important to note that even a lasting political agreement on the reopening of the Strait of Hormuz will not mean immediate shipping of crude oil. The logistics of resuming export flows will need to be managed, from demining the strait itself to realigning refinery supply chains and suppressed demand4. Further, due to the closure of the Strait of Hormuz, some oil fields in West Asia had to be shut-in. Following the US-Iran preliminary agreement to cease hostilities and the possible reopening of the Strait of Hormuz, these oil fields may be restarted to resume oil supply. One analyst estimates that the affected oil fields could “get back to 70% of prior production within three months and to 90% within six months”5. Thus, if the Strait of Hormuz remains open, Hormuz-linked oil and gas supply may remain uneven and only reach pre-war levels towards the end of 2026 or even 20276.

The closure of the Strait of Hormuz has not only raised oil prices but also affected other parts of the global economy, including Malaysia’s economy. It set off a chain reaction. For example, the closure has affected energy markets, fertiliser markets, and the food supply chain. Malaysia is not spared from this chain reaction, despite a common public assumption that, as an oil-producing country, it should be insulated from the impact. This article discusses why Malaysia cannot escape the consequences of the Strait of Hormuz crisis and why it will remain exposed in the future if it depends on crude oil supplies from Hormuz-linked countries. This article also discusses the reactions of selected governments to the energy crisis. Primary data used in this article are drawn from UN Comtrade bilateral trade data for 20257.

How Malaysia Came to Depend on the Strait of Hormuz

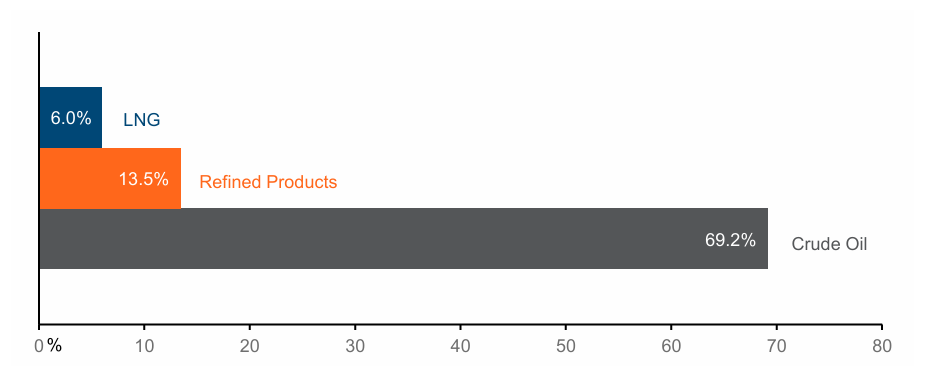

Figure 1: Share of Malaysia's petroleum imports sourced from Hormuz-linked countries, by product, 2025

Figure 1 above shows that in 2025, 69.2% of Malaysia's crude oil imports originated from Hormuz-linked countries. For refined products, the Hormuz share stood at 13.5%, and for liquefied natural gas (LNG) it was 6.0%, giving a combined share of 32.7% across all three product categories.

The wide gap between the crude oil figure and the other two products reflects the evolution of Malaysia's energy system over time8. Most Malaysian refineries are configured to process heavier sour crude oil, while domestic light sweet crude is sold abroad at premium prices9. Domestic refineries have been estimated to contribute to 66.3% of Malaysia's refined product output in 2025, with the remainder sourced from Singapore, South Korea and China10. Malaysia has ranked among the fifth-largest LNG exporters globally since 201911, which explains why its share of LNG imports from Hormuz-linked countries remains small. PETRONAS has confirmed that nearly 40% of Malaysia's crude oil requirements transit through the Strait, underscoring where the country's energy vulnerability is most concentrated12.

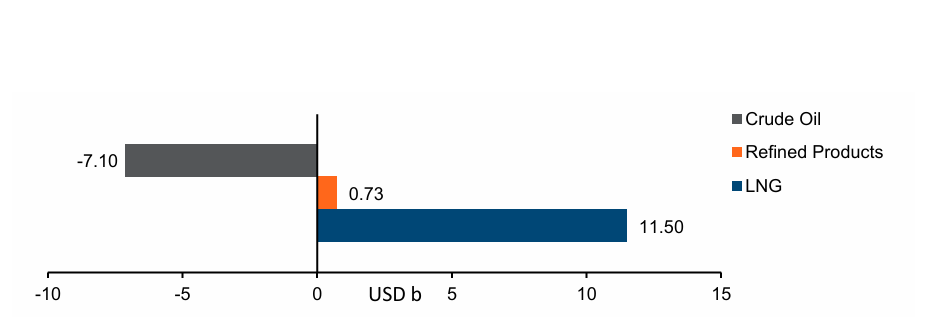

Figure 2: Petroleum trade balance of Malaysia, by product, 2025 (USD billion)

Figure 2 above shows what this import structure costs and earns in trade balance terms. Crude oil recorded a deficit of USD7.10b in 2025, as Malaysia imports more than it exports. Refined products returned a modest surplus of USD0.73b. LNG posted the largest surplus of USD11.50b, reflecting Malaysia’s status as a major gas exporter. Thus, the potential reopening of the Strait of Hormuz would mean that Malaysia would gain access to crude from Hormuz-linked countries.

The LNG surplus means that Malaysia's overall petroleum trade is positive, but this balance may change depending on how countries react to the disruption at the Strait of Hormuz. On the crude side, a closure compresses import supply and widens the deficit. On the gas side, the risk is indirect as the closure restricts Qatar and UAE trade, which together account for almost one-fifth of global LNG trade13. This tightens Asian spot LNG prices and strains the domestic gas supply balance that underpins Malaysia's power sector14.

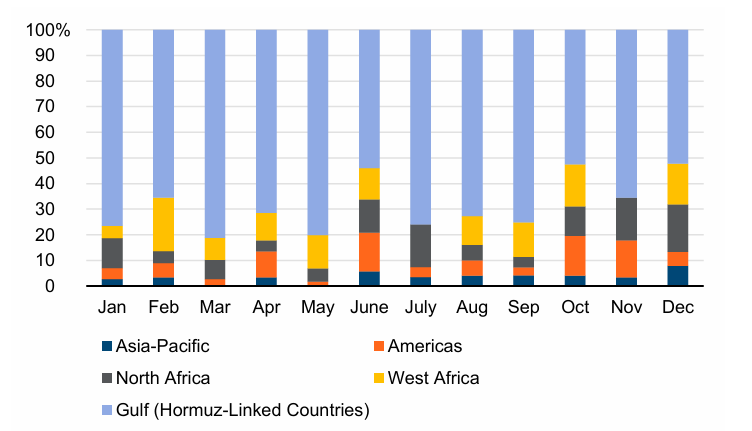

Figure 3: Monthly crude oil imports of Malaysia, by source region, 2025 (%)

Figure 3 above shows the monthly share of Malaysia's crude oil imports by source region throughout 2025. The Gulf dominates every month, averaging 69.2% annually, peaking at 81.2% in March and falling to 51.7% in October. West Africa, North Africa, and the Americas account for the remainder in varying proportions, while Asia-Pacific sources contribute a consistently small share.

The Gulf share never disappears, confirming that Gulf crude is a structural constant in Malaysia's refinery feedstock rather than an occasional source15. PETRONAS has secured additional supply from West Africa and Latin America as a contingency measure16, though these represent a supplement rather than a replacement. When alternative suppliers are used, longer shipping routes carry higher freight and insurance costs that feed directly into domestic fuel prices, and Hormuz disruptions have already contributed to crude prices rising by nearly 40%17. One partial buffer has been the large overhang of Russian and Iranian crude oil that had accumulated at sea in the months before the February 2026 conflict, barrels from the sanctioned shadow fleet effectively warehoused on the water and subsequently redirected into Asian spot markets once the Strait closed, dampening what would otherwise have been a sharper price hike18.

Asia Shares the Same Grip

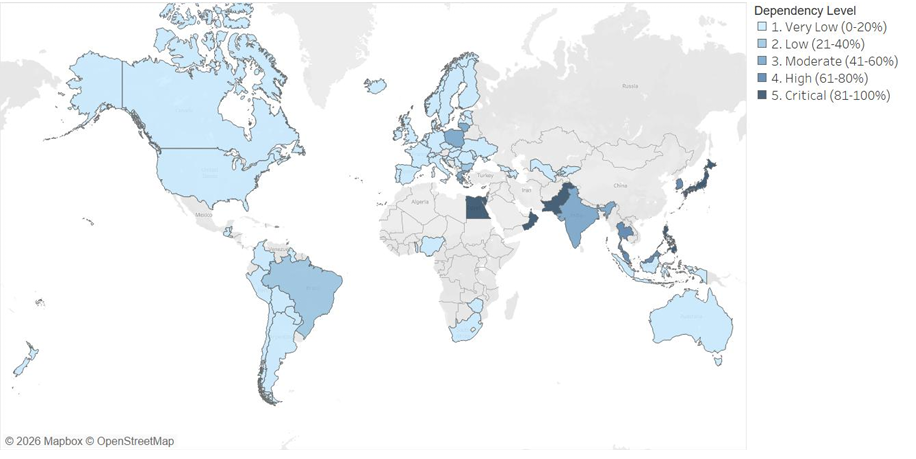

Figure 4: Crude oil import dependency on Hormuz-linked countries, by reporting country, 2025 (%)

Figure 4 above plots crude oil dependency on the Strait of Hormuz across all countries reporting bilateral trade data to UN Comtrade in 202519. Nevertheless, the highest dependency-level countries stretch from the Arabian Peninsula into South Asia, and onward to Japan and the Philippines. Europe and the Americas have comparatively lower dependency levels. Dependency on the Strait of Hormuz is unevenly distributed, with Asian economies (including Malaysia) feeling its closure more than others.

In 2025, approximately 34% of global crude oil trade (nearly 15 mb/d) passed through the Strait, with most of the volumes destined for Asian markets, as China and India alone received 44% of all crude exports transiting the waterway20. This highlights how heavily the world's two most populous economies depend on this single maritime chokepoint. In the same year, around 78% of Middle Eastern crude exports went to China, together with Japan, South Korea, and Taiwan21. Thus, the reopening of the Strait of Hormuz would be welcomed by economies worldwide, particularly Asian economies. Nevertheless, research has indicated that China’s significant reserves and coal power have contributed towards its ability to weather the disruption of approximately 55% of its crude imports and 30% of its LNG imports22.

Meanwhile, Viet Nam sources 88% of its crude from the Persian Gulf23. In South Asia, Bangladesh sources almost 100% of its crude imports and 71% of its LNG through the Strait24, placing it alongside Pakistan at the highest level of vulnerability and with no viable alternative crude route.

Global Trade Policy Responses

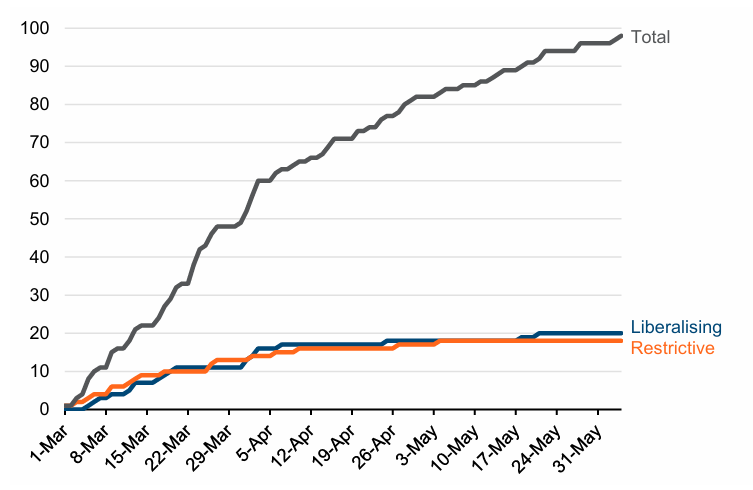

When Iran closed the Strait of Hormuz to most trade in response to the war launched by the US and Israel, the global supply of oil, LNG, and other essential goods was severely diminished. Economies around the world were threatened as a critical ingredient in their industries, power grids, farms, and transportation systems became suddenly scarcer. In the months following the strait’s closure, governments responded with a wide variety of trade policies designed to shield their economies from the damaging effects of shortages. Some countries sought to counteract the dwindling supply of essential goods on the world market by artificially increasing the amount of those goods available to their own domestic markets. It is estimated that up to 18 countries imposed barriers to exports25. Figure 5 below shows the early proliferation of these restrictive export barriers, the liberalising of imports to ease trade, and other related policy measures.

Among the most stringent of these barriers was Thailand’s 6 March 2026 ban on exports of petroleum products and liquid petroleum gas to all countries except Laos and Myanmar, on whom Thailand relies for hydropower and LNG26. To understand Thailand’s urgency in enacting such a restrictive policy, it is useful to examine its position in the global market for petroleum products. According to UN COMTRADE data, Thailand exported just over 3.5m tonnes of petroleum products in 2025 and imported just over 1.5m tonnes27. With imports shrunken by the Hormuz crisis, Thailand had little margin for error between its petroleum product output and the input levels to which its economy is accustomed.

In contrast, South Korea exported over 52m tonnes and imported less than 10m tonnes of petroleum products in 2025. Though South Korea is unlikely to match that export number in 2026 given this year’s crude shortages, the country’s large exports relative to Thailand’s mean that it has far more to lose by forcing its exporters into the domestic market – especially given the inflated prices they would fetch overseas. Hence, while South Korea also took steps to curtail fuel exports this year, it did so with a lighter touch: limiting exports of diesel, gasoline, and kerosene to their 2025 levels28. By effectively holding exports constant, it is possible that Seoul sought to balance refiners' interests by allowing them to reap the benefits of higher global prices while preventing them from directing excess product overseas to the detriment of South Korean consumers.

India imposed an even less restrictive export barrier on 26 March 2026 when it increased its tax on diesel exports29. Again, the relationship between exports and imports is instructive: India exported over 42m tonnes of petroleum products in 2025, and imported just over 4m tonnes. Despite being faced with crude shortages similar to South Korean refiners, Indian refiners had a far greater opportunity to profit from high global prices, and the Indian government chose to extract that surplus rather than obstruct it. In fact, that additional revenue was at least partially beneficial to harder-hit portions of the Indian economy, as the government reduced duties on imports of ammonium nitrate and certain chemical and plastic products several days later30.

India’s lowered duties represent an alternative means of increasing domestic supply of scarce goods, altogether different from the three preceding approaches: rather than try to keep the goods in, this next set of approaches seeks to make it easier for the goods to enter in the first place. For example, the US has lowered sanctions barriers on both Iranian and Russian crude oil and oil products31. Though the sanctions reversals came at a cost to longstanding US geopolitical goals regarding both Iran and Russia, in the immediate term, easing sanctions was a cheap way to combat rising fuel prices.

Viet Nam removed a restriction of its own in March, permitting two additional companies, besides the state-owned oil and gas outfit, to import and export crude. In general, India, the Philippines, South Korea, and Viet Nam have all reduced duties or tariffs on goods impacted by the Hormuz Strait closure32. Like the US sanctions reversals, these import easing efforts generally trade long-term goals, like tax revenue, for immediate relief. However, that swap carries a different cost for different countries. India and South Korea, whose refiners are earning more on their exports due to the Hormuz situation, are much better placed to offset the cost of the import easing than are the Philippines and Viet Nam, who each imported almost 8m tonnes of petroleum products in 2025 yet exported only about 6,000 and 370,000 tonnes, respectively.

Figure 5: Cumulative number of new trade measures implemented after 28 February 2026, by day

Note: Some of the measures expired before June 4. Expiration dates are not reflected in the chart.

After the initial supply shock, many governments moved from restricting exports and easing imports to increasing fuel subsidies, granting temporary tax credits to especially vulnerable industries, launching clean energy investment programmes, and buying and releasing strategic reserves. Measures that made importing products easier sought to improve the domestic supply of key goods. Some other measures sought to favour domestic energy production over foreign supplies and to sponsor the construction of new domestic capacities in areas such as renewable energy. These investments could improve the post-crisis trade prospects for the countries involved – including Australia, India, Japan, Malaysia, New Zealand, the Philippines, and South Korea – by helping their economies bounce back faster and giving their exporters a boost above competitors33.

Such domestic assistance policies, especially with regard to small and medium-sized enterprises (SMEs), have been the focus of Malaysia’s economic response to the crisis. These policies include an exemption on import duties for Malaysian SMEs seeking to reimport goods the crisis prevented them from exporting, announced on 20 April 2026 and valid through the end of 202634. Bank Negara followed this exemption with a RM5b SME Stabilisation Relief Facility, which will provide loans up to RM750,000 at a maximum interest rate of 3.75% through the end of this year to SMEs negatively impacted by the crisis.35 This month, the Malaysian government has also announced a long-term commitment from Russia to supply gas, oil, and petroleum, as well as a deal with Turkmenistan offering expanded gas access36.

Thus, it remains to be seen whether more restrictive measures, rather than liberalising measures, would be useful for countries moving forward, given the reopening of the Strait of Hormuz. Experience from measures imposed at the height of the Covid-19 pandemic has shown that both restrictive and liberalising measures can be imposed temporarily, thereby meeting domestic needs while facilitating global trade through the smooth movement of goods and services once the need subsides.

Conclusion

Despite the planned reopening of the Strait of Hormuz, Malaysia will likely still experience the impact of its closure this year. Further, ongoing negotiations between the US and Iran require significant issues to be addressed, creating a sensitive agreement in principle that could hold or break down in the near-term. The Strait of Hormuz has never been merely a shipping lane. For Malaysia and much of Asia, it is one of the lifelines on which economic stability depends. The reality is that Malaysia cannot escape the consequences of this crisis, and future insulation remains unlikely for as long as it depends on crude oil supplies from Hormuz-linked countries. Further, this article discusses the reactions of selected governments to the energy crisis – both restrictive and liberalising measures. Thus, this paper analyses the trade relationships impacting Malaysia and the shifting nature of those relationships as countries around the world respond with a variety of restrictive and liberalising trade policies. It sheds light, too, on Malaysian SME support programmes for a less vulnerable present and energy supply diversification for a more resilient future.

.avif)